DOI: https://doi.org/10.34069/AI/2024.83.11.10

Volume 13 - Issue 83: 126-141 / November, 2024

How to Cite:

Tkach, O., Saienko, V., Vader, T., Morhulets, O., & Bielikova, N. (2024). Responsible management in administrative management: Innovative approaches and forecasts. Amazonia Investiga, 13(83), 126-141. https://doi.org/10.34069/AI/2024.83.11.10

Responsible management in administrative management: Innovative approaches and forecasts

Gestión Responsable en la Gestión Administrativa: Enfoques Innovadores y Previsiones

Received: October 1, 2024 Accepted: November 29, 2024

Written by:

Oleg Tkach

https://orcid.org/0000-0001-9833-9544

Doctor of Economics, Professor, Department of Management and Marketing, Faculty of Economics, Vasyl Stefanyk Precarpathian National University, Ivano-Frankivsk, Ukraine.

WoS Researcher ID: KVB-8147-2024 - Email: oleg.tkach@pnu.edu.ua

Volodymyr Saienko

https://orcid.org/0000-0003-2736-0017

DSc. in Organization and Management, Professor, Department of Innovation Management, Faculty of Social Sciences, Academy of Applied Sciences – Academy of Management and Administration in Opole, Opole, Poland. WoS Researcher ID: J-9099-2016 - Email: saienko22@gmail.com

Tetyana Vader

https://orcid.org/0009-0008-1744-6646

Ph.D. in Public Administration, Senior Lecturer, Department of Marketing and Business Administration, Educational and Scientific Institute of Economics and Management, Pryazovsky State Technical University, Dnipro, Ukraine. WoS Researcher ID: IAN-3730-2023 - Email: tnvpost@gmail.com

Oksana Morhulets

https://orcid.org/0000-0001-6530-1478

Doctor of Economic Sciences, Professor, National University of Life and Environmental Sciences of Ukraine, Education and Research Institute of Continuing Education and Tourism, Kyiv, Ukraine.

WoS Researcher ID: P-9911-2016 - Email: morgulets_oks@nubip.edu.ua

Nadiia Bielikova

https://orcid.org/0000-0002-5082-2905

Doctor of Economic Sciences, Professor, Research Center for Industrial Problems of Development of the National Academy of Sciences of Ukraine; Department of Management, Logistics and Innovation, Simon Kuznets Kharkiv National University of Economics, Kharkiv, Ukraine.

WoS Researcher ID: JTS-8522-2023 - Email: nadezdabelikova@gmail.com

Abstract

In modern business, a rational combination of administrative and responsible management is an integrated management instrument promoting adaptive development and implementation of innovative technologies. The study aims to generalise approaches to defining the essence and role of responsible management in the administrative management system and clarify the factors that ensure the efficiency of management processes. To achieve the research objective, factor analysis was used to systematise the main factors that influence the effectiveness of the responsible business management system. As a result of the factor analysis on the example of PJSC CB “Privat Bank”, it was found that for today's business, it is essential to analyse a significant set of indicators and study them in dynamics. Two factors were explicitly identified for the selected company: the factor of strategic development and business reliability, which includes the banking business reliability ratio, the equity protection ratio, the maximum risk ratio, the rating of the reliability of banking products, the rating of public confidence in the bank; as well as the factor of investment attractiveness of the business, which includes the capital multiplier coefficient, the standard of significant risks. In general, the combination of administrative and responsible management can open up significant additional opportunities for effective development.

Keywords: responsible management, resource-saving, administrative management, social responsibility, factor analysis, innovative approaches to management.

Resumen

En la empresa moderna, la combinación racional de gestión administrativa y gestión responsable es un instrumento integrado de gestión que promueve el desarrollo adaptativo y la aplicación de tecnologías innovadoras. El estudio pretende generalizar los enfoques para definir la esencia y el papel de la gestión responsable en el sistema de gestión administrativa y aclarar los factores que garantizan la eficacia de los procesos de gestión. Para alcanzar el objetivo de la investigación, se utilizó el análisis factorial para sistematizar los principales factores que influyen en la eficacia del sistema de gestión empresarial responsable. Como resultado del análisis factorial sobre el ejemplo de PJSC CB «Privat Bank», se constató que para la empresa actual es esencial analizar un conjunto significativo de indicadores y estudiarlos en dinámica. Para la empresa seleccionada se identificaron explícitamente dos factores: el factor de desarrollo estratégico y fiabilidad del negocio, que incluye el coeficiente de fiabilidad del negocio bancario, el coeficiente de protección del capital propio, el coeficiente de riesgo máximo, la calificación de la fiabilidad de los productos bancarios, la calificación de la confianza del público en el banco; así como el factor de atractivo inversor del negocio, que incluye el coeficiente multiplicador del capital, el estándar de riesgos significativos. En general, la combinación de una gestión administrativa y responsable puede abrir importantes oportunidades adicionales para un desarrollo eficaz.

Palabras clave: gestión responsable, ahorro de recursos, gestión administrativa, responsabilidad social, análisis factorial, enfoques innovadores de gestión.

Introduction

Context

Responsibility in management originates from the paradigm of human existence, in which any results of one's actions are directly related to him as a performer of a specific task and a source of transformations in the world. The ability of an individual to take responsibility for his or her actions is related to conscious prognosticating, i.e. the ability to predict the consequences of specific influences and to act purposefully, considering the analysis of the prospects for the development of events.

Research problem

The main problem with implementing responsible management principles in a company is that only some companies have sufficient financial resources to implement an appropriate responsibility policy. In addition, tracking performance in this area requires a significant investment in setting goals, monitoring indicators and adapting the approach to constantly changing environmental conditions, which not all organisations can afford.

Research Focus is focused on identifying the peculiarities of implementing a responsible management system in the classical practice of administrative management in modern business development.

Definition of the Problem

In administrative management, responsibility is inextricably linked to functional roles in the organisational structure: different positions in the company's hierarchy are associated with powers and imply different areas and degrees of responsibility for the people involved in implementing their tasks.

Objectives and Significance of the Study

The research aim is to summarise approaches to understanding the essence and significance of responsible management in the administrative management system and specify the factors that ensure the effectiveness of management processes in modern administrative management.

To achieve this goal, the following tasks should be solved: determining the specifics of building a responsible management system; to specify the features of combining administrative and responsible management against the background of the introduction of modern innovative management technologies; to identify business development factors that allow assessing the effectiveness of responsible management.

Literature review

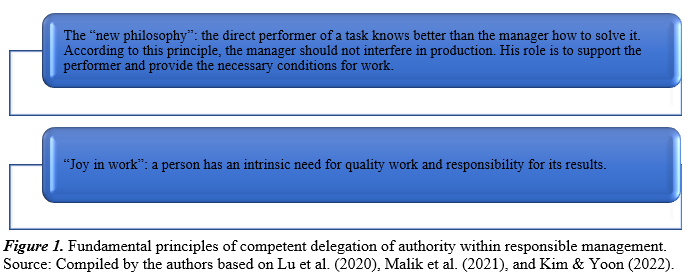

Specialists in the field of quality management have identified the fundamental principles underlying the competent delegation of authority and the creation of a responsible management system (AlHamad et al., 2022; Baraja & Chaniago, 2023; Ivanov et al., 2024), as shown in Figure 1.

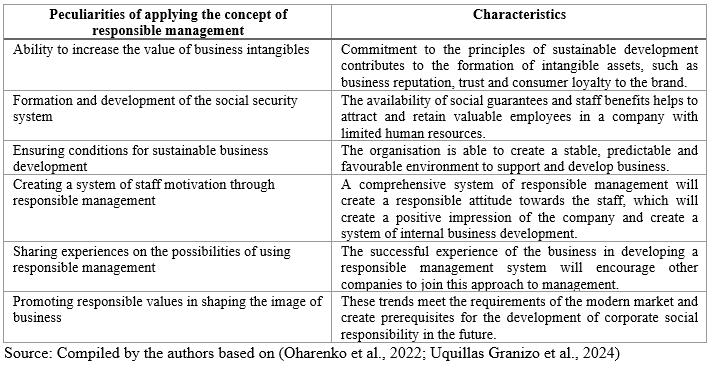

Delegation of responsibility within an organisation is the process of transferring tasks, competences and partially powers from a direct manager to subordinates. On the one hand, this allows the manager to get rid of some of the functions and focus on implementing the company's strategy. On the other hand, delegation is a tool for motivating staff, linking increased responsibility with access to power and personal development. In today's business environment, special attention is also paid to corporate social responsibility, which involves the voluntary participation of companies in improving the life of society, caring for the rights of employees, protecting the environment and developing the territory where their business operates. The founder of the theory of corporate social responsibility is considered to be the American economist G. Bowen (1908-1989), who in his 1953 book “The Social Responsibility of the Businessman” (Bowen, 2013) expressed its essence as “the implementation of policies, decision-making, or adherence to a line of behaviour that is desirable from the standpoint of the goals and values of society” (Barbosa et al., 2020; Gil-Gomez et al., 2020). Pryimak et al. (2024) argue that innovative approaches to risk management are pivotal for improving decision-making processes and enhancing public administration's adaptability. Their study highlights the dual challenge of integrating technological solutions while addressing bureaucratic impediments and resource constraints, especially in the Ukrainian context. Subsequently, the theory of corporate social responsibility has become widespread in the business environment, along with the recognition of globalisation and the prospects for further development of modern administrative management designed to address global environmental and social issues, as well as the emergence of the concept of sustainable development, which would “meet the needs of the living without depriving future generations of the opportunity to meet their needs” (Aleksieienko et al., 2020; Lam et al., 2021; Vdovichen et al., 2023). Corporate responsibility as a concept has evolved under pressure from trade unions, environmental activists and public representatives interested in the sustainable development of individual companies, nature and society (Sayed, 2023; Srijani et al., 2023; Verbivska et al., 2023). However, over time, it has come to be perceived as a competitive advantage in the process of creating an attractive image of an organisation in the eyes of the public. Summarising the views of researchers on the implementation of the responsible management concept, it becomes possible to systematise its advantages and peculiarities of application in the modern business environment (Table 1).

Table 1.

Advantages and features of applying the concept of responsible management by modern business

The peculiarities of the application of responsible and administrative management, presented in Table 1, allow to effectively manage an organisation or enterprise in the modern business environment, based on the principles of organisation of managerial innovations, i.e. on the guidelines developed by theory and practice, which should be followed in the process of innovation management. Knowledge of and adherence to the principles can improve the efficiency of preparation and implementation of managerial innovations and ultimately increase the effectiveness of administrative activities. There are general and technological principles for organising managerial innovations. The general principles include the principle of controllability of the innovation process, the principle of relevance of innovations, and the principle of systematic innovation. The principle of controllability of the innovation process means that there are objective prerequisites for exerting managerial influence on the process of development and implementation of innovations. Implementation of innovations is not a spontaneous process. Achieving an innovative effect requires coordinated actions to reduce deviations from the chosen course. This is necessary because the innovation process is not automatically regulated. The task of purposeful management of the innovation process is to ensure that the actual state of the innovation process is in line with the desired, planned state. The solution to this task involves the implementation of all management functions, from planning to controlling changes. The operational performance of these functions should be assigned to the relevant competent service (body) in the administrative institution. The principle of the relevance of innovations means that managerial innovations should be seen as the result of the organisational development of the administrative activity system. The current state of the management system is reflected in the content of the planned organisational changes. For this reason, the innovation project should be organically linked to the existing needs of the management body to improve the structure and methods of management. Based on the literature analysis, it is worth noting that the policy of responsible management is based on a set of principles that determine the interaction between the company, on the one hand, and employees, shareholders, partners, the community, and the environment, on the other. The current situation confirms the need to intensify efforts to adopt responsible management, as this will help solve global problems and maximise the efficiency of organisations and businesses.

Methodology

Data Selection

During the study, a certain sequence of stages was carried out, which allowed reasonable and systematic results to be obtained. At the first stage, the specifics of building a responsible management system for modern business were determined, considering the possibilities of combining responsible and administrative management. The next step was to identify the peculiarities of combining administrative and responsible management against the background of the introduction of modern innovative management technologies. Next, the article specifies the factors of business development that make it possible to assess the effectiveness of management responsible.

Literary sources for the study were selected based on their relevance, with the main focus on works published over the past five years. This made it possible to consider current trends in the development of administrative management within the framework of modern management theory.

Objectivity in the selection of sources was ensured by involving works published in different countries and focusing on keywords rather than specific authors. The keywords used for the literature search include administrative management, responsible management, and modern theories of business management.

Data Analysis

The basic research method chosen was bibliometric analysis, which allows us to draw reasonable conclusions based on the analysis of scientific sources. The scientific basis for the study was selected by searching the main databases of Web of Science and Scopus. In the process of conducting the research and selecting scientific sources, the time period for searching the database was determined from January 2019 to October 2024 to better match the continuity and completeness of the research conducted over the past 5 years. It was the analysis of scientific publications for this period that allowed us to identify the most relevant trends in the development of modern responsible and administrative management.

The literature was selected using the following keywords: “responsible management”, “modern trends in administrative management”, “new approaches to the formation of the concept of responsible management”, and “responsible management for modern business”. As a result of applying all these search conditions and selecting scientific sources, 65 of the most relevant publications were selected. It is also worth emphasising the wide geography of the scientific search; publications of scientists from different countries were analysed, which allowed us to identify global trends in the development of modern responsible and administrative management.

Instruments and Procedures

The main research tools are based on the analysis of the experience of using innovative administrative management tools by companies and the generalisation of this experience to formulate recommendations on the opportunities and risks of applying the latest procedures in the management of enterprises with a focus on responsible management. Innovative tools may vary significantly depending on the specific business, but the system of innovative management itself involves the introduction of modern digital technologies to facilitate the construction of a management system. First of all, we analysed the opportunities that arise for responsible management in the process of implementing planning, organisational and control functions. The proposed tools for implementing innovative development of the administrative management system may be useful primarily for managers of large companies interested in improving management systems and forming a system of corporate responsibility of business. As a separate method of determining the factors of business development that allow assessing the effectiveness of responsible management, the factor analysis was chosen, which allows systematising data on the state and development of the business into groups of factors that will directly reflect the effectiveness of responsible management. The selection of indicators for further factor analysis was based on the analysis of the direct results of business activities, such as the PJSCB Privat Bank. The statistical characteristics of the resulting factor model were also analysed, which prove that the model provides adequate results and that the conclusions drawn on its basis can be considered representative. Accordingly, based on the factor analysis, it can be argued that the implementation experience can be useful for most business representatives who combine responsible and administrative management or plan to implement responsible management approaches. In addition, it should be emphasised that the initial set of basic indicators for the implementation of factor analysis may be unique for each individual business and take into account its industry specifics, current financial position or key development targets.

Limitations

The study is not significantly limited by the research sources or information on the company's financial condition. However, it should assess the effectiveness of responsible management based on internal qualitative and quantitative development indicators, which are not publicly available and may constitute a commercial secret. Factor analysis is a fairly versatile research tool, but it has certain limitations that should be taken into account when implementing the study. In particular, attention should be paid to the selection of initial data for further factor analysis. The initial data should follow a normal distribution law and be reliable, i.e., taken from official sources, particularly financial statements or other official documents.

Findings

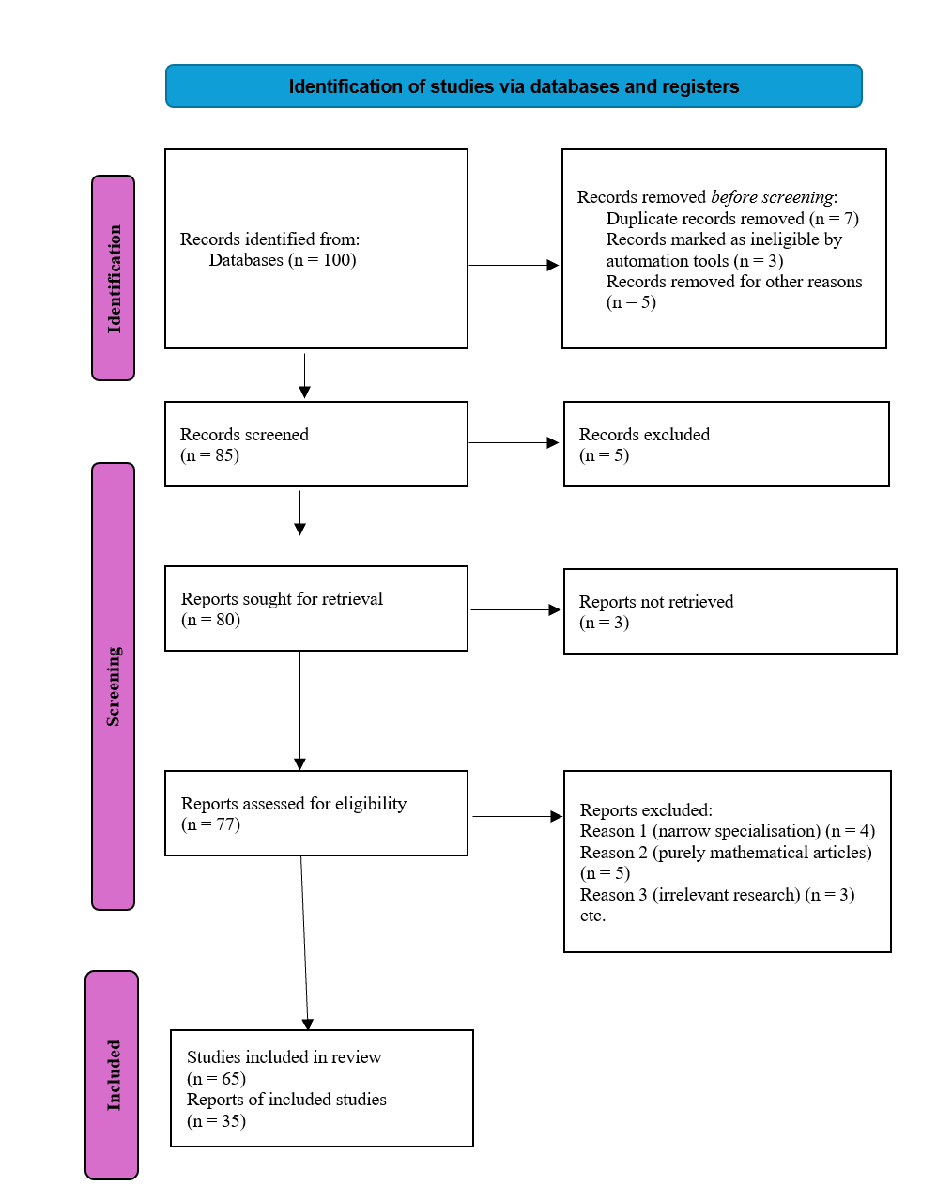

The problem of implementing the latest approaches to responsible and administrative management requires analysis of a significant number of scientific sources. These sources were selected and processed according to the PRISMA scheme, as shown in Figure 2.

In total, 100 sources of scientific literature were selected for the study. Still, for various reasons (inconsistency of the research object, duplication, narrow specialisation of certain studies), 65 sources were retained for direct use in the research process, fully meeting the requirements for sources for the study established above. In the selected scientific sources, the emphasis was placed on those publications that mainly relate to the development of administrative management in modern conditions.

The global community has always been interested in ensuring the most efficient and economical use of various resources. This issue has become particularly relevant today, as the linear economic growth caused in the last century has provoked several social problems, which can be solved by transitioning to a closed-loop economy (or circular economy). A closed-loop economy reflects the economic activity of society and even a set of market relations based on the renewal of resources. Along with the growing trends in the circular economy, managing production in the new environment is becoming increasingly important. The development of a new field, responsible management, based on integrating international standards in organisational management, has been devoted to solving this problem (Abbas et al., 2020; Barykin et al., 2021; Bryson & George, 2020).

The specifics of responsible management can be reflected in the principles of a company's policy that are making the transition to a circular economy and are aimed mainly at the following essential tasks (Chychun et al., 2023; Mariono & Sabar, 2023; Pushkina, 2024):

Fig. 2. Scheme of selection of literature sources for the study.

As mentioned above, the concept of "responsible management" is relatively new in the literature. It is reflected mainly in the studies of foreign authors whose research considers both the concept's main provisions and the strategy for its development.

In recent years, the concept of integrated management has prevailed, but there are significant differences between it and the concept of responsible management, which combines the specifics of responsible and administrative management (Mura, 2022).

According to the most relevant and innovative approaches to implementing innovative management, responsibility for the social impact of management activities is an essential element of management. Managers should achieve a positive social effect as one of their primary responsibilities by actively identifying social needs and turning them into business opportunities. Thus, responsible management of an organisation or any structure is a way of planning, organising and evaluating the organisation's activities with due regard to the interests of the global environment for the development and prosperity of both present and future generations. With the development of scientific thought in the context of management theory, one can see how the concept of responsible management has been improving and, in recent years, has begun to transform into management using the latest innovative technologies. The contribution of scientists in the current review provides a wide range of ideas for the development of responsible management.

At the beginning of the 21st century, the importance of responsible management has grown exponentially. Management scholars have a broad consensus that responsible management is a sustainable trend. Time will tell whether it is simply a new aspect that will become part of the usual understanding of management science or the next step in the evolution towards the field of top management (Okpebenyo et al., 2024; Riabov & Riabova, 2021; Storozhyk, 2024).

Tretiak et al. (2024) emphasize that an interdisciplinary approach to paradigmatic evaluation is essential for improving decision-making processes in local public management. They propose integrating empirical data with methodological innovation to enhance administrative practices and forecast more effective management outcomes. Modern management, which is mainly focused on business adaptation to an unstable external environment, involves significant changes in the system of administrative management implementation. Accordingly, attention should be paid to the current trends in management processes that are typical for a business that is developing in today's environment:

Since today an essential component in the management of any enterprise or organisation is a sustainable development policy, which is also a tool for the transition to a circular economy, its principles, in line with the concept of responsible management, should help the organisation avoid, reduce and control the harmful impact of its activities on society and the population, comply with applicable legal requirements and be part of a trend that customers value. Sustainable development considers the concept of quality of life from a complex economic, social and environmental perspective, promoting the idea of a balance between economic development, social justice, efficient use and preservation of the environment (Iastremska et al., 2024; Lapuente & Van de Walle, 2020; Leo, 2024). A key element of sustainable development is reconciling development and resource-saving opportunities, which contributes to an integrated decision-making process at the global, regional, national, or local levels.

Thus, adopting and systematically implementing a set of methods for implementing the principle of responsibility in management can help achieve optimal results for the benefit of all stakeholders.

In order to ensure the effective development and implementation of a responsible management system to address social and governance issues, it is necessary to balance service tasks and powers. Thus, the goals of economic and social policy to address social problems in the concept of responsible management should include the following provisions (Bachynskyi, 2024; Saxena et al., 2024):

From the above, the responsible management policy is based on a set of principles that define the interaction between the company, on the one hand, and employees, shareholders, partners, the community and the environment, on the other. The current situation confirms the need to intensify efforts to adopt responsible management, as this will help solve global problems and maximise the efficiency of organisations and businesses.

Thus, in today's conditions, administrative management is a field of management that focuses on the organisation and coordination of various aspects of an organisation or enterprise. Its arsenal has many tools and methods that allow it to obtain a positive result.

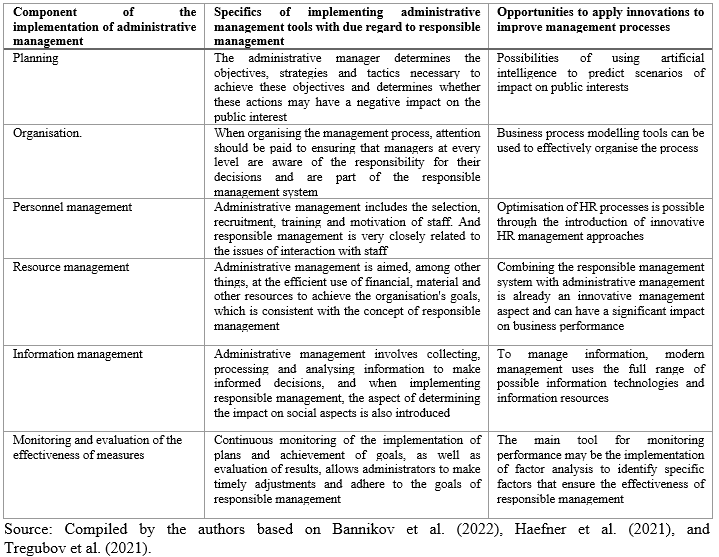

Table 2 shows some administrative management features in actively implementing responsible management approaches. It is proposed to consider these features through the classical management functions, but with an awareness of how they are implemented in modern conditions.

Table 2.

Specifics of the combination of administrative and responsible management against the background of the introduction of modern innovative management technologies.

The peculiarities of the application of responsible and administrative management, presented in Table 2, allow for effective management of an organisation or enterprise in the modern business environment based on the principles of organisation of managerial innovations, i.e. on the guidelines developed by theory and practice, which should be followed in the process of innovation management. Knowledge of and adherence to the principles can improve the efficiency of preparation and implementation of managerial innovations and ultimately increase the effectiveness of administrative activities. There are general and technological principles for organising managerial innovations.

The general principles include (Lam et al., 2021; Sayed, 2023): the principle of controllability of the innovation process, the principle of relevance of innovations, and the principle of systemic innovation.

The principle of controllability of the innovation process means that there are objective prerequisites for managerial influence on the process of development and implementation of innovations. Implementation of innovations is not a spontaneous process. Achieving an innovative effect requires coordinated actions to reduce deviations from the chosen course. This is necessary because the innovation process is not automatically regulated. The task of purposeful management of the innovation process is to ensure that the actual state of the innovation process is in line with the desired, planned state.

The solution to this task involves the implementation of all management functions, from planning to controlling changes. The operational performance of these functions should be assigned to the relevant competent service (body) in the administrative institution.

The principle of the relevance of innovations means that managerial innovations should be seen as the result of organisational development of the administrative system. The current state of the management system is reflected in the content of the planned organisational changes. For this reason, the innovation project should be organically linked to the existing needs of the management body to improve the structure and methods of management.

One of the pioneering companies in the field of responsible management in Ukraine was PJSC CB PrivatBank, which has been adhering to the principles of responsible management for more than ten years.

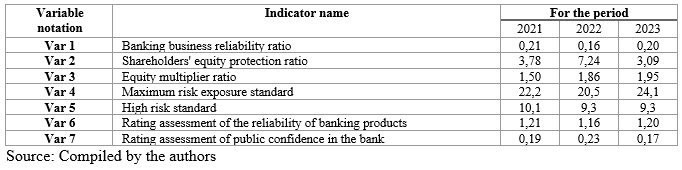

It is on its example that it is logical to analyse the factors of administrative and responsible management performance using factor analysis. Table 3 shows the initial data for factor analysis - key indicators of management performance.

Table 3.

Initial data for factor analysis - key performance indicators of the management of PJSC CB “PrivatBank”

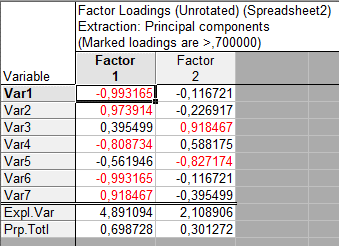

The results of the factor analysis are shown in Fig. 3.

Fig. 3. Distribution of factors because of factor analysis of the effectiveness of the combination of administrative and responsible management on the example of PJSC CB “PrivatBank”

Source: Compiled by the authors.

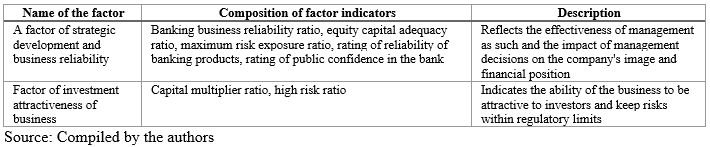

According to Fig. 3, it becomes possible to identify two factors that allow assessing the effectiveness of the combination of administrative and responsible management. A description of the set of indicators for each of the factors is provided in Table 4.

Table 4.

Results of the factor analysis of performance indicators of the combination of administrative and responsible management of PJSC CB “PrivatBank”

The factor analysis tool can be adapted to each specific type of business, but it should be emphasised that its use makes it possible to fully systematise and group key indicators of a particular business's development, form a system for monitoring the effectiveness of management methods and styles and assess the rationality of the chosen management strategy.

Discussion

The study primarily identifies the latest approaches to combining administrative and responsible management tools. At the same time, responsible management is seen as an opportunity to adapt to the latest conditions of business development with innovative digital technologies, which makes it possible to significantly improve the conditions for business development and ensure an increase in the efficiency of using available resources.

Modern administrative management allows wider opportunities for improvement and development of an organisation based on its own, primarily administrative, resources that mobilise its synergistic effect. Implementation of the administrative management system allows for the discovery of unused management elements and the increase of the management system's synergistic effect in the organisation.

Administrative management in European and Asian companies has evolved from the development of a classical administrative management system to lean manufacturing, information technology, and further quality management systems (Komalasari et al., 2020; Lăzăroiu et al., 2020; Fatima & Elbanna, 2023).

Therefore, it should be emphasised that the administrative management system is primary. Any management improvement in companies around the world usually begins with establishing an administrative system. It is the foundation of effective management. However, it should be emphasised that administrative management, if not implemented rationally, can create additional risks for management processes and significantly affect staff productivity. All these aspects should be taken into account in the process of planning actions to implement management systems. In addition, certain risks are created by the irrational use of digital technologies in response to trends in the modern economic space. Accordingly, business representatives should focus on the most active implementation of digital tools and consider the appropriateness of using a particular tool.

Modern administrative management on the verge of 2023-2024 allows for the implementation of a process approach to management and the use of its capabilities (Baraja & Chaniago, 2023). This is important for small organisations, as it solves the problem of manageability, which increases as they grow and develop.

It is even more critical for medium and large organisations with many lines of business that need more flexibility due to the complexity of their management. This idea was proved in the course of the research and factor analysis based on the data of PJSC CB “PrivatBank”.

The application of the process approach allows for an audit of the existing management system at enterprises in order to separate all end-to-end processes of production of goods and services from each other (Bryhinets et al., 2020; Rozsa et al., 2021; Scherer & Voegtlin, 2020). However, researchers need to focus on adapting administrative management to responsible management approaches when building a comprehensive management system focused on optimising the use of all types of resources and the optimal implementation of innovations. However, many innovations only produce serious results if they are based on a modern administrative management system that uses the possibilities of a responsible approach and rational use of various types of resources.

If an enterprise wants to improve management efficiency, it should start by identifying gaps in the existing management system and creating the conditions for further improvement.

Innovative administrative management can be a reasonable basis for mastering responsible management methods, the use of information technology, and the application of quality systems (Bacq & Aguilera, 2022; Wiesböck & Hess, 2020; Dmytriyev et al., 2021). However, at the same time, administrative management allows you to move to the organisation of careful production of goods or provision of services. Lean manufacturing is a revolutionary, breakthrough approach to management in general and quality management in particular, as it ensures the long-term competitiveness of enterprises without significant capital investment. Accordingly, lean manufacturing can be considered the first step towards implementing responsible management, which most scholars do not mention today or focus on creating an administrative management system with elements of responsible management. Drawing from the innovative risk management strategies in public administration, Pryimak et al. (2024) emphasize the critical role of integrating advanced mechanisms at multiple governance levels to foster sustainable and efficient management practices. Their findings highlight the necessity for adaptive strategies tailored to regional and local contexts, underlining the interplay between decentralization and resource optimization to achieve overarching strategic goals within public administration frameworks.

In general, most researchers prove that one of the trends in modern innovative administrative management is introducing a responsible management system (Azmat et al., 2023; Marques & Gomes, 2020; Pharmacista, 2024). However, it is worth supplementing the opinions of scientists with an emphasis on modern opportunities for the development of administrative management, taking into account the latest digital technologies that can facilitate the process of creating and developing a new management system based on a combination of administrative and responsible management concepts. This can be achieved by introducing internal quality control systems or creating additional areas for optimising HR, ensuring responsible management conditions and attracting more employees to the new system.

The issue of expanding the administrative management toolkit is currently being considered by scholars in different countries and from different perspectives. One group of researchers (Redko et al., 2024; Wiesböck & Hess, 2020) focuses on the fact that successful enterprise management requires precise regulation of all administrative processes. Other researchers (Sembiyeva et al., 2023; Shkarlet et al., 2020), on the contrary, suggest that it is essential for modern businesses to build a flexible management system that will allow them to adapt to the environment and quickly adjust to market requirements. As a result of the author's study, it is difficult to disagree with the second group of researchers since today's business operates in a highly volatile environment, and the ability to develop and adapt becomes the key to effective functioning and the possibility of obtaining positive changes. Accordingly, a flexible and adaptive management system can more efficiently respond to changes in the external environment and create the basis for rapid adaptation to new conditions. In this case, the business will have more opportunities to overcome the negative impact of the external environment and create preconditions for further development.

Another controversial issue in analyzing the innovative development of administrative management is the integration of digital technologies into contemporary management systems. Buriak and Petchenko (2021), Kaldygozova (2024), and Prylypko (2023) emphasize that the necessity of adopting the latest digital technologies in management is evident. However, it is crucial to consider the risks, including significant initial costs and the substantial restructuring of company personnel. This process requires the recruitment of IT specialists and the training of existing staff to adapt effectively to new digital tools implemented within the organization.Cybersecurity is an important aspect highlighted in various studies (Tkachova et al., 2023; Tiurina et al., 2022; Padilla-Lozano & Collazzo, 2022). In addition, it is worth supporting the opinion of scholars who emphasise the need to pay special attention to building a data protection and information security system when planning to develop an administrative management system using digital platforms. Particular attention should be paid to protecting customer and counterparty data and developing a reliable cybersecurity system since the reputation and image of a company largely depend on the seriousness of its attitude to information protection. At the same time, cybersecurity issues should be secondary to developing or updating management approaches, as management efficiency should remain the primary goal, and cybersecurity is a prerequisite for creating a secure business environment.

Conclusion

Modern administrative management requires new approaches to developing the management system, which is what responsible management is becoming today. The study found that for most companies, it is relevant and appropriate to introduce a combination of administrative and responsible management, as it makes it possible to perform social functions and ensure effective internal development processes.

It can be argued that a flexible working model based on responsible management is becoming a trend today, as a development of which a growing number of companies around the world are moving to flexible working models, such as remote work, flexible working hours and other alternatives to the traditional office environment. This requires new approaches to human resources management and workflow organisation but also yields positive results in resource savings.

While conducting a factor analysis on the example of PJSC CB “Privat Bank”, it was found that it is essential for today's business to analyse a significant set of indicators and study them in dynamics. Two factors were explicitly identified for the selected company: the factor of strategic development and business reliability, which includes the banking business reliability ratio, the equity protection ratio, the maximum risk ratio, the rating of the reliability of banking products, the rating of public confidence in the bank; as well as the factor of investment attractiveness of the business, which includes the capital multiplier ratio, the standard of significant risks.

Since responsible management involves close cooperation with the staff, working with the staff to determine the optimal methods and tools of responsible management can be highlighted as a promising area for further research on the subject of the article.

Specific contributions of the study

Responsible management in modern management theory opens up new opportunities for businesses to actively use the latest tools in the management process.

The main result of the study is that, using factor analysis, it is proved that modern tools of responsible management can be used in business development and management decision-making. In addition, innovative approaches to administrative management can positively impact the formation of the company's image in the market and indirectly affect the financial condition by attracting additional investors, creating the possibility of more reasonable investment financing, expanding markets, etc.

Implications for the findings

For business practice and business development in the current environment, responsible management provides an opportunity to focus on strategic development and set strategic goals that will meet the requirements of the internal business environment and take into account most aspects of socially responsible business growth. In the innovative management theory, responsible management is viewed not only as a system of business management rules but also as a concept and strategy for the company's development. It is a philosophy that influences the formation of strategic goals and tactical measures to achieve them.

Bibliographic references

Abbas, J., Zhang, Q., Hussain, I., Akram, S., Afaq, A., & Shad, M. A. (2020). Sustainable innovation in small medium enterprises: The impact of knowledge management on organizational innovation through a mediation analysis by using SEM approach. Sustainability, 12(6), 2407. https://doi.org/10.3390/su12062407

Aleksieienko, I., Leliuk, S., & Poltinina, O. (2020). Information and communication support of project management processes and enterprise value. Development Management, 18(3), 1–13. https://doi.org/10.21511/dm.18(3).2020.01

AlHamad, A., Alshurideh, M., Alomari, K., Kurdi, B. A., Alzoubi, H., Hamouche, S., & Al-Hawary, S. (2022). The effect of electronic human resources management on organizational health of telecommuni-cations companies in Jordan. International Journal of Data and Network Science, 6(2), 429–438. https://doi.org/10.5267/j.ijdns.2021.12.011

Alrowwad, A., Abualoush, S. H., & Masa’deh, R. (2020). Innovation and intellectual capital as intermediary variables among transformational leadership, transactional leadership, and organizational performance. Journal of Management Development, 39(2), 196–222. https://doi.org/10.1108/jmd-02-2019-0062

Asgarov, B. M., & Mustafayev, M. H. (2024). Systematic Analysis of the use of Innovative Approaches in Operational and Investigative Activities: The Republic of Azerbaijan Case. Future Economics & Law, 4(3), 34-46. https://doi.org/10.57125/FEL.2024.09.25.03

Azmat, F., Jain, A., & Sridharan, B. (2023). Responsible management education in business schools: Are we there yet? Journal of Business Research, 157(113518), 113518. https://doi.org/10.1016/j.jbusres.2022.113518

Bachynskyi, O.-S. (2024). Mechanism for the Formation and Implementation of HR Policy: The Global Experience. Futurity of Social Sciences, 2(2), 62–78. https://doi.org/10.57125/FS.2024.06.20.04

Bacq, S., & Aguilera, R. V. (2022). Stakeholder governance for responsible innovation: A theory of value creation, appropriation, and distribution. The Journal of Management Studies, 59(1), 29–60. https://doi.org/10.1111/joms.12746

Bannikov, V., Lobunets, T., Buriak, I., Maslyhan, O., & Shevchuk, L. (2022). On the question of the role of project management in the digital transformation of small and medium-sized businesses: essence and innovative potential. Amazonia Investiga, 11(55), 334–343. https://doi.org/10.34069/ai/2022.55.07.35

Bannikova, K. (2022). To the question of migration of capital and labour force of Ukraine: Forecast of future trends. Futurity Economics&Law, 2(2), 32-41. https://doi.org/10.57125/FEL.2022.06.25.04

Baraja, H., & Chaniago, H. (2023). Investigation of Business Capital and Product Innovation in Culinary Business Development: Evidence from a Densely Populated City. Futurity Economics&Law, 3(3), 97–114. https://doi.org/10.57125/FEL.2023.09.25.06

Barbosa, M., Castañeda -Ayarza, J. A., & Lombardo Ferreira, D. H. (2020). Sustainable Strategic Management (GES): Sustainability in small business. Journal of Cleaner Production, 258(120880), 120880. https://doi.org/10.1016/j.jclepro.2020.120880

Barykin, S. Y., Bochkarev, A. A., Dobronravin, E., & Sergeev, S. M. (2021). The place and role of digital twin in supply chain management. Academy of Strategic Management Journal, 20(Special Issue 2), 1-24. https://www.abacademies.org/articles/the-place-and-role-of-digital-twin-in-supply-chain-management.pdf

Bowen, H. R. (2013). Social Responsibilities of the Businessman. University of Iowa Press. https://doi.org/10.2307/j.ctt20q1w8f

Bryhinets, O., Svoboda, I., Shevchuk, R., Kotukh, Y., & Radich, V. (2020). Public value management and new public governance as modern approaches to the development of public administration. Revista San Gregorio, 1(42), 205-214. https://doi.org/10.36097/rsan.v1i42.1568

Bryson, J., & George, B. (2020). Strategic management in public administration. In Oxford Research Encyclopedia of Politics. Oxford University Press. https://doi.org/10.1093/acrefore/9780190228637.013.1396

Buriak, I., & Petchenko, M. (2021). Analysis of the dilemmas of building an accounting system for the needs of future economic management. Futurity Economics&Law, 1(1), 17–23. https://doi.org/10.57125/FEL.2021.03.25.3

Chychun, V., Chaplynska, N., Shpatakova, O., Pankova, A., & Saienko, V. (2023). Effective management in the remote work environment. Journal of System and Management Sciences, 13(3), 244-257. https://doi.org/10.33168/JSMS.2023.0317

Cichosz, M., Wallenburg, C. M., & Knemeyer, A. M. (2020). Digital transformation at logistics service providers: barriers, success factors and leading practices. International Journal of Logistics Management, 31(2), 209–238. https://doi.org/10.1108/ijlm-08-2019-0229

Criado, J. I., & Guevara-Gómez, A. (2021). Public sector, open innovation, and collaborative governance in lockdown times. A research of Spanish cases during the COVID-19 crisis. Transforming Government People Process and Policy, 15(4), 612–626. https://doi.org/10.1108/tg-08-2020-0242

Dmytriyev, S. D., Freeman, R. E., & Hörisch, J. (2021). The relationship between stakeholder theory and corporate social responsibility: Differences, similarities, and implications for social issues in management. Journal of Management Studies, 58(6), 1441-1470. https://doi.org/10.1111/joms.12684

Dooranov, A., Orozonova, A., & Alamanova, C. (2022). The Economic Basis for the Training of Specialists in the Field of Personal Management: Prospects for the Future. Futurity Economics&Law, 2(1), 35–49. https://doi.org/10.57125/FEL.2022.03.25.04

Fatima, T., & Elbanna, S. (2023). Corporate social responsibility (CSR) implementation: A review and a research agenda towards an integrative framework. Journal of Business Ethics, 183(1), 105–121. https://doi.org/10.1007/s10551-022-05047-8

Gil-Gomez, H., Guerola-Navarro, V., Oltra-Badenes, R., & Lozano-Quilis, J. A. (2020). Customer relationship management: digital transformation and sustainable business model innovation. Economic Research-Ekonomska Istraživanja, 33(1), 2733–2750. https://doi.org/10.1080/1331677x.2019.1676283

Haefner, N., Wincent, J., Parida, V., & Gassmann, O. (2021). Artificial intelligence and innovation management: A review, framework, and research agenda✰. Technological Forecasting and Social Change, 162, 120392. https://doi.org/10.1016/j.techfore.2020.120392

Iastremska, O., Bielikova, N., Kozlova, I., & Herashchenko, I. (2024). Strategic Management of Innovative Development of Enterprises According to the Experience Economy Model: A Review. Futurity Economics&Law, 4(3), 158–176. https://doi.org/10.57125/FEL.2024.09.25.10

Ivanov, A., Remzina, N., Kolinets, L., Koldovskiy, A., & Odnolko, V. (2024). Development and management of the tourist and recreation complex as a strategic direction of the tourism economy in the system of sustainable development. AD ALTA: Journal of Interdisciplinary Research, 14(1), 252–256. https://doi.org/10.33543/j.140140.252256

Kaldygozova, S. (2024). Using mobile technologies in distance learning: A Scoping Review. E-Learning Innovations Journal, 2(1), 4–22. https://doi.org/10.57125/ELIJ.2024.03.25.01

Kim, S., & Yoon, A. (2022). Analyzing Active Fund Managers’ Commitment to ESG: Evidence from the United Nations Principles for Responsible Investment. Management Science, 69(2), 723-1322. https://doi.org/10.1287/mnsc.2022.4394

Komalasari, K., Arafat, Y., & Mulyadi, M. (2020). Principal’s Management Competencies in Improving the Quality of Education. Journal of Social Work and Science Education, 1(2), 181-193. https://doi.org/10.52690/jswse.v1i2.47

Lam, L., Nguyen, P., Le, N., & Tran, K. (2021). The Relation among Organizational Culture, Knowledge Management, and Innovation Capability: Its Implication for Open Innovation. Journal of Open Innovation: Technology, Market, and Complexity, 7(1), 66. https://doi.org/10.3390/joitmc7010066

Lapuente, V., & Van de Walle, S. (2020). The effects of new public management on the quality of public services. Governance, 33(3), 461–475. https://doi.org/10.1111/gove.12502

Lăzăroiu, G., Ionescu, L., Andronie, M., & Dijmărescu, I. (2020). Sustainability Management and Performance in the Urban Corporate Economy: A Systematic Literature Review. Sustainability, 12(18), 7705. https://doi.org/10.3390/su12187705

Leo, J. G. (2024). The Macroeconomic Impact of Crude Oil Price Fluctuations in Nigeria. Futurity of Social Sciences, 2(3), 147–181. https://doi.org/10.57125/fs.2024.09.20.09

Lu, J., Liang, M., Zhang, C., Rong, D., Guan, H., Mazeikaite, K., & Streimikis, J. (2020). Assessment of corporate social responsibility by addressing sustainable development goals. Corporate Social Responsibility and Environmental Management, 28(2), 686-703. https://doi.org/10.1002/csr.2081

Malik, S. Y., Hayat Mughal, Y., Azam, T., Cao, Y., WAN, Z., ZHU, H., & Thurasamy, R. (2021). Corporate Social Responsibility, Green Human Resources Management, and Sustainable Performance: Is Organizational Citizenship Behavior towards Environment the Missing Link? Sustainability, 13(3), 1044. https://doi.org/10.3390/su13031044

Mariono, A., & Sabar. (2023). The Influence of School Management Information Systems and Teacher’s Social Competence on the Parent Satisfaction of Junior High School Students. Futurity Education, 3(2), 79–104. https://doi.org/10.57125/FED.2023.06.25.05

Marques, T. M. G., & Gomes, J. F. S. (2020). Responsible leadership andversus responsible management. In Research Handbook of Responsible Management (pp. 138–154). Edward Elgar Publishing. https://doi.org/10.4337/9781788971966.00017

Mura, L. (2022). The philosophy of personnel management of small and Medium-sized businesses in Slovakia. Futurity Philosophy, 1(3), 27–39. https://doi.org/10.57125/FP.2022.09.30.02

Oharenko V. M., Pokatayeva O.V., Diachenko M.D. (2022). The management aspect of training future heads of educational institutions for economic activity. Baltic Journal of Economic Studies, 8(1), 111–117. https://doi.org/10.30525/2256-0742/2022-8-1-111-117

Okpebenyo, W., Ogini, S., & Ileleji, P. A. (2024). Working Capital Management and the Performance of SMEs in Delta North. Futurity of Social Sciences, 2(3), 106–121. https://doi.org/10.57125/fs.2024.09.20.07

Padilla-Lozano, C. P., & Collazzo, P. (2022). Corporate social responsibility, green innovation and competitiveness-causality in manufacturing. Competitiveness Review: An International Business Journal, 32(7), 21-39. https://www.emerald.com/insight/content/doi/10.1108/CR-12-2020-0160/full/html

Pharmacista, G. (2024). Legal Responsibility of Companies That are Negligent in Managing Waste Which Causes Environmental Damage. Fox Justi: Journal of Legal Studies, 14(02), 143-152. https://ejournal.seaninstitute.or.id/index.php/Justi/article/view/4328

Pryimak, M., Kalyta, L., Sokolov, M., Vladyslav, K., & Krasnykov, Y. (2024). Innovative approaches to risk management in the field of public administration in Ukraine: Prospects and limitations. Amazonia Investiga, 13(74), 308–322. https://doi.org/10.34069/AI/2024.74.02.26

Prylypko, V. (2023). Current issues and problems of legal training of specialists in non-legal specialities. Futurity Economics & Law, 3(1), 53–62.

Pushkina, N. (2024). Developing Social Skills Through Rhythmic Gymnastics in American sport. Futurity of Social Sciences, 2(2), 79–102. https://doi.org/10.57125/FS.2024.06.20.05

Redko, K., Riznyk, D., Nikolaiev, S., Yatsenko, O., & Shuplat, O. (2024). The Role of Investment in Creating a Sustainable Financial Future: Strategies and Tools. Futurity Economics&Law, 4(3), 20–33. https://doi.org/10.57125/FEL.2024.09.25.02

Riabov, I., & Riabova, T. (2021). Development of the creative sector of the world economy: trends for the future. Futurity Economics&Law, 1(4), 12–18. https://doi.org/10.57125/FEL.2021.12.25.02

Rozsa, Z., Belas, J., Jr, Khan, K. A., & Zvarikova, K. (2021). Corporate social responsibility and essential factors of personnel risk management in SMEs. Polish Journal of Management Studies, 23(2), 449–463. https://doi.org/10.17512/pjms.2021.23.2.27

Saxena, P. K., Seetharaman, A., & Shawarikar, G. (2024). Factors that influence sustainable innovation in organizations: A systematic literature review. Sustainability, 16(12), 4978. https://doi.org/10.3390/su16124978

Sayed, R. (2023). Exploring Cultural Influences on Project Management Approaches in Global Business Development. Futurity of Social Sciences, 1(4), 38–60. https://doi.org/10.57125/FS.2023.12.20.02

Scherer, A. G., & Voegtlin, C. (2020). Corporate governance for responsible innovation: Approaches to corporate governance and their implications for sustainable development. The Academy of Management Perspectives, 34(2), 182–208. https://doi.org/10.5465/amp.2017.0175

Sembiyeva, L., Zhagyparova, A., Zhusupov, E., & Bekbolsynova, A. (2023). Impact of Investments in Green Technologies on Energy Security and Sustainable Development in the Future. Futurity of Social Sciences, 1(4), 61–74. https://doi.org/10.57125/FS.2023.12.20.03

Serikova, M., Sembiyeva, L., Mussina, A., Kuchukova, N., & Nurumov, A. (2018). The institutional model of tax administration and aspects of its development. Investment Management and Financial Innovations, 15(3), 283–293. https://doi.org/10.21511/imfi.15(3).2018.23

Shkarlet, S., Dubyna, M., Shtyrkhun, K., & Verbivska, L. (2020). Transformation of the paradigm of the economic entities development in digital economy. WSEAS Transactions on Environment and Development, 16, 413–422. https://doi.org/10.37394/232015.2020.16.41

Srijani, N., Aisyah, S., Kadeni, & Sri Hariani, L. (2023). The Sustainability of Sharia MSMEs in the Halal Industry of Indonesia: Funding, Protection, and Sharia Principles. Futurity Economics&Law, 3(4), 32–47. https://doi.org/10.57125/FEL.2023.12.25.03

Storozhyk, M. (2024). Philosophy of future: analytical overview of interaction between education, science, and artificial intelligence in the context of contemporary challenges. Futurity Philosophy, 3(1), 23–47. https://doi.org/10.57125/FP.2024.03.30.02

Tiurina, A., Nahornyi, V., Ruban, O., Tymoshenko, M., Vedenieiev, V., & Terentieva, N. (2022). Problems and prospects of human capital development in post-industrial society. Postmodern Openings, 13(3), 412–424. https://doi.org/10.18662/po/13.3/497

Tkachova, N., Saienko, V., Bezena, I., Tur, O., Shkurat, I., & Sydorenko, N. (2023). Modern trends in the local governments' activities. A D Alta: Journal of Interdisciplinary Research, 13(3), 111-118. https://www.academia.edu/62054395/MODERN_TRENDS_IN_THE_LOCAL_GOVERNMENTS_ACTIVITIES

Tregubov, O., Podrieza, S., Hoi, N., Ivanova, T., & Kulinich, T. (2021). Green economy development under the financial crisis: The world practice and experience. Estudios de Economía Aplicada, 39(9). https://www.proquest.com/openview/a9fc8938d90341a9906219a65c817439/1?pq-origsite=gscholar&cbl=2034867

Tretiak, O. A., Khmelnykov, A. O., Batrymenko, O. V., Karashchuk, M., & Husieva, N. (2024). Paradigmatic dimensions of local public management research: The path to reliable managerial decisions. Amazonia Investiga, 13(76), 228–235. https://doi.org/10.34069/AI/2024.76.04.18

Uquillas Granizo, G. G., Mostacero, S. J., & Puente Riofrío, M. I. (2024). Exploring the competencies, phases and dimensions of municipal administrative management towards sustainability: A systematic review. Sustainability, 16(14), 5991. https://doi.org/10.3390/su16145991

Vdovichen, A., Vdovichena, O., Chychun, V., Zelich, V., & Saienko, V. (2023). Communication management for the successful promotion of goods and services in conditions of instability: Attempts at scientific reflection. International Journal of Organizational Leadership, 12(First Special2023), 37–65. https://doi.org/10.33844/ijol.2023.60364

Verbivska, L., Zhuk, O., Ievsieieva, O., Kuchmiiova, T., & Saienko, V. (2023). The role of e-commerce in stimulating innovative business development in the conditions of European integration. Financial and Credit Activity: Problems of Theory and Practice, 3(50), 330–340. https://doi.org/10.55643/fcaptp.3.50.2023.3930

Wiesböck, F., & Hess, T. (2020). Digital innovations: Embedding in organizations. Electronic Markets, 30(1), 75–86. https://doi.org/10.1007/s12525-019-00364-9

https://amazoniainvestiga.info/ ISSN 2322- 6307

This article presents no conflicts of interest. This article is licensed under the Creative Commons Attribution 4.0 International License (CC BY 4.0). Reproduction, distribution, and public communication of the work, as well as the creation of derivative works, are permitted provided that the original source is cited.