Social Outcomes of Corporate Governance: Evidence from the Food Industry of Pakistan

Resultados sociales del gobierno corporativo: evidencia de la industria alimentaria de Pakistán

Abstract

Social and environmental problems are becoming strategic concerns for the managers in the current business scenario because it is challenging their sustainability. Here the need arises to respond to this changing phenomenon accordingly. In this regard social impact of corporate governance has not yet been explored where it can play a role of driver of excellence in terms of social performance and it is required to be studied. To check the existing situation, this study has been conducted where the social impact of corporate governance has been explored in the food Industry of Pakistan. Questionnaires have been filled from 176 managers working in six food producing firms listed in Pakistan Stock Exchange (PSX). Structural Equation Modeling based partial least square (PLS) has been used where Smart PLS has been used for model estimation. Results are supporting the stakeholder theory as Nestle Pakistan and Engro Foods are driving social excellence through corporate governance practices, where the corporations are showing strong positive relationships of corporate governance practices with stakeholders management, environmental integrity and protection, social cohesion and equity while insignificant relationship exists between strategic proactivity and corporate governance practices as people are resistant to change and innovation. The relationships can be explored in other industries like Oil and gas, Chemicals and Construction etc.

keyword

Corporate Governance Practices, Stakeholder Management, Environmental Protection and Social Cohesion.

Resumen

Los problemas sociales y ambientales se están convirtiendo en preocupaciones estratégicas para los gerentes en el escenario comercial actual porque está desafiando su sostenibilidad. Aquí surge la necesidad de responder a este fenómeno cambiante en consecuencia. En este sentido, aún no se ha explorado el impacto social del gobierno corporativo, donde puede desempeñar un papel de impulsor de excelencia en términos de desempeño social y debe ser estudiado. Para verificar la situación existente, este estudio se realizó donde se ha explorado el impacto social del gobierno corporativo en la industria alimentaria de Pakistán. Se han completado cuestionarios de 176 gerentes que trabajan en seis empresas productoras de alimentos que cotizan en la Bolsa de Valores de Pakistán (PSX). Se ha utilizado el mínimo cuadrado parcial (PLS) basado en modelado de ecuaciones estructurales donde se ha utilizado Smart PLS para la estimación del modelo. Los resultados respaldan la teoría de las partes interesadas, ya que Nestlé Pakistan y Engro Foods están impulsando la excelencia social a través de prácticas de gobierno corporativo, donde las corporaciones muestran fuertes relaciones positivas de prácticas de gobierno corporativo con la gestión de los interesados, integridad y protección ambiental, cohesión social y equidad, mientras que existe una relación insignificante entre la proactividad estratégica y las prácticas de gobierno corporativo, ya que las personas son resistentes al cambio y la innovación. Las relaciones se pueden explorar en otras industrias como el petróleo y el gas, los productos químicos y la construcción, etc.

Palabras clave

prácticas de gobierno corporativo, gestión de partes interesadas, protección ambiental y cohesión social.

Introduction

Economic activities of the corporations are resulting into various environmental problems day by day. These problems are increasing with the passage of time and exerting legal, political and social pressures on the corporations to control it (Galdeano-Go´mezet al., 2008). According Henri and Journeault (2008), it is becoming a strategic concern for the managers to address immediately because it can affect corporation’s sustainability. Here the need arises to respond to this changing phenomenon accordingly. Firstly, corporations must have to incorporate social purpose into their vision and mission. Environment protection and employee loyalty must also be the part of its purpose. Economic sustainability and serving society can best be achieved by incorporating these values in governance systems. Organizational focus should be beyond its operating performances and legal implementation. It should be based on shared values and objectives. Then they are needed to adopt such mechanism of direction and control which takes into account all the stakeholders rather than the shareholders only (Wilson, 2000).

Corporate governance is such an area which is widely being researched by academicians. Literature is full of governance researches. But most of the studies focused on principal-agent problem. Social impact of corporate governance has not yet been explored and it is required to be analyzed (Academy of Management, 2014).According to study of Audretsch & Lehmann (2011), corporate governance is a well-known and well researched concept of Economics, Accounting &Finance, Management and Law etc. While studies of Bebchuk & WeIsbach (2010) and Brown & Beekes et al. (2010-11) explored practices of corporate governance incorporated by giant corporations. Major proportion of research is done on the corporate governance practices of public companies having thousands of employees and listed in stock exchange. On contrary, more focus is required to study the corporate governance practices done by small non listed corporations.

Concern of the century is how the corporations understand themselves relative to community at large. Shareholder is the part of the purpose of the corporation not a whole purpose. They are the one part of the society; the other parts would include decreasing damage to the environment and improving lives. Jenkins (2009) claims, that corporation are paying immense attention on the development of society and environment friendliness as a key to achieve competitive advantage. Corporations and society as a whole can be truly represented by care and share only (Academy of Management, 2014).

However, in contrast to the impact of corporate governance practices on financial performance of firms, current study is focusing on the effects of corporate governance with perspective of social performance that is not only beneficial for shareholders but for stakeholders as well.

Literature Review

Corporate Governance

The mechanism of corporate governance is actually from hiring and accountability of board of directors and auditors by shareholders with a purpose to provide direction and control to all affairs of the corporation (Cadbury, 1992).Corporate governance consists of procedures through which fund providers assure themselves of getting return on their investment (Shleifer & Vishny, 1997). This view of corporate governance works with the separation of ownership and control (Jensen & Meckling, 1976) where fund providers have to make it sure that their funds are utilized properly in their best interest by the managers. Corporate governance was defined as a system to regulate external (shareholding policy and outside block holding etc.) as well as internal (size of board, remunerations and other internal policies etc.) affairs of an organization (Agrawl & Knoeber, 1996). While Serrat, O. (2011) define corporate governance is a very interesting way. According to her study, whenever people and structures interact with each other to address the common societal and organizational needs they need direction and control. So, corporate governance is the framework of laws and regulations to provide them required direction and control.

The concept of corporate governance has been expanded in the recent past where the community has also been taken into consideration the stakeholder perspective (Jansen, 2001). It is a change from shareholder perspective to stakeholder perspective. It has been evolved from the profit maximization approach to social responsibility approach where the social impact of corporate governance is getting attention of both the practitioners and researchers. Businesses cannot earn profits without the support and integration of stakeholders, because in a socioeconomic system businesses and society depends on each other for profitability and responsibility (Halal, 2000). Corporate governance not only a guiding and controlling framework to secure the commitment of stakeholders but a well-structured mechanism to channelize the skills, knowledge and expertise of stakeholders to avail the shared benefits at maximum. It not only constrained to utilization of skill, knowledge etc. but also deals with property rights of stakeholders, management of their associations and devising effective incentives plans to reduce agency issues. Furthermore, scope of corporate governance is extended to the responsibility allocation, improvements and innovations in processes (Suzanne, C. Neil et al. 2006).

Attiya Y. Javid and Robina Iqbal (2010) claimed in their study that for sustainable organizational growth it is essential to link the performance with good corporate governance practices. In emerging markets well-implemented corporate governance practices, successfully attaining the desired objectives of public policies. Every public limited have to publish the corporate governance report as per SECP Corporate Governance Code 2001 requirements. So, corporate governance is the latest most researched potential subject now a day in Pakistan.

Social Outcomes

There is still no single definition of corporate social responsibility. It means showing concern for all the stakeholders. Businesses agree to show ethical behavior and work for economic development by simultaneously providing quality life to its employees in terms of social cohesion and integrity and society at large in terms of environment integrity and protection (World Business Council for Sustainable Development, 1999).From literature review it is found that shared vision, employee involvement, capital management, proactive strategy, stakeholder management, innovation, CSR integrated strategy formulation (Hart, 1995; Aragon-Correa, 1998; Christmann, 2000; Anderson & Bateman, 2000; Buysse &Verbeke, 2003; Bansal, 2005; Jenkins, 2009; Sharma et al., 2007; and CSR integrated strategy formulation (Cordano and Frieze, 2000) etc. is the range of competencies required to adopt a proactive CSR strategy to achieve the desired social outcomes. Study of Castka et al., (2004) revealed that until and unless, social responsibility is incorporated into the objectives of the businesses and its governance system, the desired results cannot be achieved. It is necessary to include social responsibility into the business strategy and governance system, where the author presented framework for social responsibility with the assumption of embedded social responsibility into the purpose of governance mechanism of the businesses.

Corporations are not only meant for getting profits and follow rules and regulations, but they have responsibility towards society at large as well (Carroll, 2000a). Corporations cannot work in isolation. Caring and sharing is the only way to success. Business is expecting something from society in terms of profits and society is also expecting something from the business and both these are the part of corporate social contract (Bowie, 1983). Carroll (1979) stated in his work thatit is the responsibility of the corporation to earn profit for shareholders, to abide by the rules and regulations, doing right things and showing concern for society. Social outcomes are evident such as social cohesion and equity etc. due to embedding the concept of corporate social responsibility (CSR) in corporate governance. In 21st century, business climate is polluted with fierce competition and for survival of the businesses, it is necessary to realize as well as respond to the social responsibilities. And businesses are trying to explore the answer of most important question that by adopting CSR focused strategy; firm can achieve the sustained socio-economic and environmental growth: a route to superior performance and competitive advantage (Dunphy, 2003; Jenkins, 2009). According to Groza et al., (2011) a firm is proactive in term of CSR when it takes the social responsibility by free will and develop the strategies on priority basis to resolves these issue.

Economic growth and prosperity, environmental integrity and protection, and social cohesion and equity are the basic principles of sustainable economic development that can be attained via adopting proactive approaches of CSR. Limited empirical research has done so that is the reason to study these variables. When researchers talk about the employees well-being (health, safety etc.), provision of career development opportunities to increase the motivation level of the workers and presenting the firm as a responsible part of the community then they actually talking about social cohesion and equity that is attained through proactive CSR strategies (European Commission, 2003). It elaborates how firms can focus on stakeholders in the workplace and in the community.

Literature on integrity and protection of environment showed agreement with the arguments that the firms having proactive approach towards social responsibility not only focus on taking innovative pollution control measures and winning the title of leader in environment protection. Despite of this their core objective is to redesign the every phase of product life cycle that will reduce the negative impacts on ecological system to minimum level (Aragon-Correa, 1998; Buysse & Verbeke, 2003). Such strategies increase the complexity level of all activities performed by the businesses to create value addition (Rutherfoord et al., 2000; Schaper, 2002).

Organizational Characteristics

For getting both profitability and responsibility simultaneously, it is important to incorporate these values into the purpose of the businesses. Firstly, the vision and mission of the businesses should fully reflect these values for its implementation. Some characteristics are required by the businesses if they want to work for society at large. Those required characteristics are shared vision and employee involvement (Andersson and Bateman, 2000), stakeholder management (Buysse and Verbeke, 2003) and strategic proactivity (Aragon-Correa, 1998). If these characteristics do businesses possess in their purpose then automatically those would be transferred to the governance mechanism and would help to show care for society. Tsai & Ghoshal (1998) defined shared vision as ac apability of the businesses to bring all its members on some common goals. This capability of the business promotes the employee creativity as well as organizational learning which are necessary to enhance the required skills and resources for formulation and implementation of effective proactive corporate social responsible strategies. Being proactive in corporate socially responsible strategy along with shared vision develop the sense of great employee involvement and enthusiasm which is essential to incorporate innovative processes in any organization (Graafland et al., 2003; Hart, 1995).

Stakeholder management is the ability of the businesses to build trust worthy and cooperative relationship with different types of stakeholders which are having direct/indirect relationship with them (Sharma and Vredenburg, 1998). By developing the strong positive relationship with stakeholders, organizations can mitigate the negatives impacts (like social and environmental etc.) that create hindrance to attain the competitive advantage. Sharma et al., (2007) study titled these impacts as “context-specific stakeholder pressures’’, that drastically influenced that value addition chain of the firm. And the firm’s ability to effectively manage the all types of stakeholders resulted in the form of high probability to be proactive in terms of corporate social responsibility (Henriques&Sadorsky, 1999; Buysse&Verbeke, 2003).

Strategic proactivity is the capacity of the businesses to anticipate and take advantage of the new opportunities of the business appearing in the environment (Sharma et al., 2007). Miles & Snow research work conducted in 1978 provides the strong grounds for the concept of strategic proactivity. According to their work, strategically proactive firms focused on incorporating the external information as well as opportunities into their production, administrative and entrepreneurial processes. Being socially responsible in innovation and creativity to attain the competitive advantage, these firms pay more attention on employee’s empowerment (Veliyath & Shortell, 1993; Starik & Rands, 1995; Aragon-Correa, 1998).

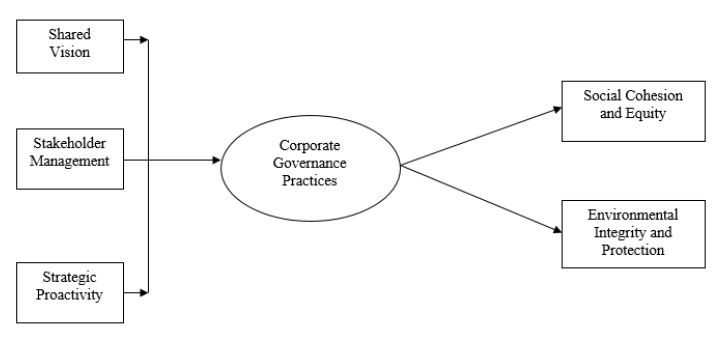

Theoretical framework

Theoretical framework contains conceptual model of the study as under:

Figure 1. Model of the Study.

H1: A shared vision capability is positively associated with the adoption of corporate governance practices.

H2: Stakeholder management is positively associated with the adoption of corporate governance practices.

H3: Strategic proactivity is positively associated with the adoption of corporate governance practices.

H4: Adoption of corporate governance practices is positively associated with social cohesion and equity.

H5: Adoption of corporate governance practices is positively associated with environmental protection and integrity.

H6: Adoption of corporate governance practices mediates the relationship between shared vision and social cohesion and equity.

H7: Adoption of corporate governance practices mediates the relationship between shared vision and environmental protection and integrity.

H8: Adoption of corporate governance practices mediates the relationship between stakeholder management and social cohesion and equity.

H9: Adoption of corporate governance practices mediates the relationship between stakeholder management and environmental protection and integrity.

H10: Adoption of corporate governance practices mediates the relationship between strategic proactivity and social cohesion and equity.

H11: Adoption of corporate governance practices mediates the relationship between strategic proactivity and environmental protection and integrity.

Methodology

Sample

Food producing firms of Pakistan listed in Karachi Stock Exchange 100 index have been considered as sample for this study. Total six firms that are listed in KSE-100 Index named as: National Foods Limited, Rafhan Maize Products Limited, Nestle Pakistan Limited. Engro Foods Limited, J.D.W. Sugar Mills Limited and Punjab Oil Mills Limited. For the sake of exploring the impact of corporate governance on social cohesion & equity and on the environment it is suitable as a sample. These firms claimed employees as their capital and commitment to environment protection. Questionnaire with a five-point likert scale (1 = “strongly disagree”, 5 =“strongly disagree”) has been used to collect data from 176 managers working in these organizations on the basis of convenience. (See Appendix at the end for details of constructs and measurement items).

According to Genier et al., (2009) food sector depends heavily on physical, human and natural resources where it is a basic human need. Due to its importance, Food sector is required to produce healthy products by focusing more on the environmental (society hygiene needs) as well as social (employee) conditions (Maloni and Brown, 2006). To check this, food industry has been taken into consideration. There is a need to scientifically test it in this industry. Uptill now corporate governance has been discussed in terms of non-financial companies as a whole. But this study is specific to the food industry.

Statistical Technique

Structural Equation Modeling based Partial least square (PLS) technique has been used which is a second generation multivariate technique (Fornell and Cha, 1994). This technique is used to explore social impact of corporate governance in food industry of Pakistan.PLS is used because it takes latent variable as weighted sum of its indicators (Chin and Newsted 1999; Fornell and Cha 1994) and use multiple regressions for its prediction (Chin 1998b; Chin and Newsted 1999; Fornell and Bookstein 1982; Fornell and Cha 1994). Smart PLS has been used for model estimation.

Results and discussion

Measurement Model

For internal consistent reliability, Cronbach’s Alpha (Cronbach 1951; Hair et al. 2011) and Composite reliability (Werts et al. 1974; Nunnally & Bernstein 1994; Tenenhaus et al. 2005) should be greater or equal to 0.60. All the constructs are fulfilling this criterion [See Table 1: Measurement Model Assessment (Internal Consistency and Convergent Validity)]. For convergent validity, Average Variance Extracted (AVE) should be greater than or equal to 0.40 (Henseler et al. 2009; Chin 2010; Hair et al. 2013). It shows that all the constructs are explain variance in their items 40 percent or above but only explain less in case of Environmental Integrity and Protection where it is explain variance in its items up to 38% which is near to 40. All the constructs are valid. All the outer loadings are assessed against greater than and equal to 0.60 criteria to include significant items. [(See Table 1: Measurement Model Assessment (Internal Consistency and Convergent Validity)].

Table 1.

Measurement Model Assessment (Internal Consistency and Convergent Validity).

..png)

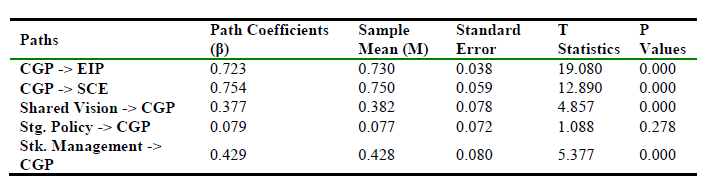

Measurement of Structural Model

It estimates the relationships among the latent variables based on theory. It uses path coefficients (β) for the strength and direction of relationship. Bootstrapping is used to check the significance of relationships. According to Hair et al.,(2013) β values lying between 0.20 and 0.30 are mostly considered significant if accompanied with R-square greater than or equal to 50%. In the study, all the t-values are found greater than 1.96 showing significant relationship but relationship between Strategic Proactivity and Corporate governance practices is statistically insignificant, where t-value is less than 1.96. Three of the hypotheses: H3, H10 and H11 are not substantiated. While strong positive and significant relationship exists among stakeholder management, shared vision, corporate governance practices, environmental Integrity and protection and social cohesion and equity [See Table 2: Path Coefficient Assessment & 3: Coefficient of Determination (R2)]

Table 2.

Path Coefficient Assessment.

Table 3.

Coefficient of Determination (R2)

.PNG)

64%, 52% and 56% variation in Corporate Governance Practices (CGP), Environmental Integrity and Protection (EIP) and Social Cohesion and Equity (SCE) is explained by the exogenous variables Shared vision , stakeholder management and proactive capability respectively.

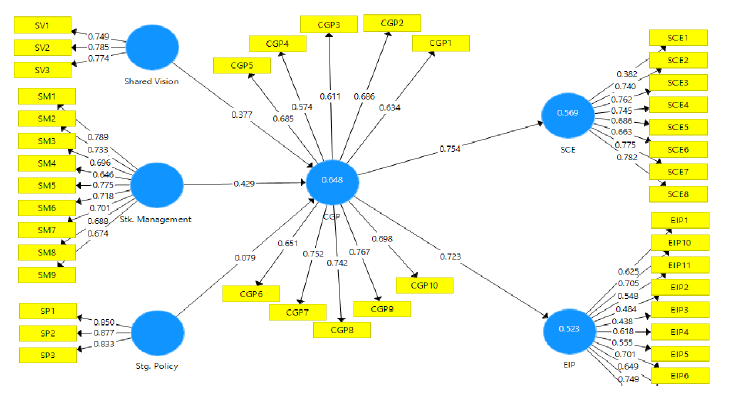

The structural representation of the model of this study is as under:

Figure 2. Summary of Hypotheses Model Calculation.

Conclusions

Objective of the study is to explore social and environmental impacts of corporate governance beyond the interests of shareholders (Academy of Management a, 2014). Multiple relationships have been explored in KSE listed food producing firms of Pakistan. Finding support the stakeholder theory (Harrison and Freeman, 1999)as Nestle Pakistan and Engro Foods are joining their hands towards society by providing quality products with managing relationships with society and employees for sustainability and environmental wellbeing. Insignificant relationship of Strategic Proactivity indicates there is lack of innovation and high resistance to change behavior prevailing in Pakistan which can further weaken the relationships. Being proactive to any cause is the key to cope the disasters created by that cause. And Pakistani firms of food industry have to seriously address this issue of lagging behind in strategic proactivity to reap the benefits of being proactive. Although corporate governance practices are the key drivers of social impact (Shahin and Zairi, 2007). Sharma et al., in his research (2007) claimed that firms failed to attain the desired level of competitive advantage if not understand the importance of stakeholder management. So, without incorporating the stakeholder management into the organizational vision/mission, positive societal effects cannot be produced. Because by managing stakeholder effectively develop the sense of responsibility in every stakeholder and this commitment level assist the firm to achieve the desired social as well environmental goals.

Limitations and Recommendations

This study is limited to the food industry of Pakistan as well as the firms listed on PSX only. On aggregate, sample size is limited. Data is collected on the basis of convenience. In-depth interviews can also provide great insights about the relationships. The relationships can be explored in other industries like Oil and gas, chemicals, construction and materials etc. comparative analysis of financial and non-financial firms can be done.