Foresight research in management accounting: scenario forecasting and a comprehensive system of expert assessment methods in agricultural holdings

ABSTRACT

Foresight research in management accounting should be aimed at solving long-term perspective issues. A set of systems and methods of expert assessment is selected or developed in the course of such studies. The managerial staff of an economic entity with the authority to make strategic decisions develop forecast scenarios taking into account the opinions of competent experts involved in the economic field under consideration. Based on the fact that there can be many options for an economic future, they jointly discuss and develop a coordinated idea of which option for future economic development is most preferable for an agricultural holding, taking into account the variability of the economic situation.The subject of the study is the improvement of management accounting in the part of Foresight research in agricultural holdings with a comprehensive assessment of the effectiveness of the management of the activities of its agricultural organizations. In modern times, agricultural holdings can change the situation through competent management accounting, since competent management accounting allows companies to consolidate their activities, thereby giving good development to agriculture, both financially and in attracting highly qualified specialists, as well as the country's food security. In accordance with this goal, the main task was determined: to develop the mechanisms of Foresight research of management accounting in agricultural holdings, for the purpose of assessing the effectiveness of management of the activities of agricultural organizations included in it. Foresight participants do not try to guess the future but build a comprehensive system of measures for the development of the agricultural holding, which allow it to be achieved; this distinguishes the difference between foresight and traditional methods of planning, forecasting and budgeting in agriculture.

keyword

Foresight, peer review, management accounting, research

Introduction

In modern times, Foresight research in management accounting should prevail over other studies, since forecast scenarios cover a large period of forecast time and include a set of measures, systems, tools and methods of expert assessment.

Management accounting in agricultural holdings should be one of the mechanisms of stability and profitability of all economic entities of the market (Kislitsky, Gogolev & Ostaev, 2018).

An agricultural holding is a set of companies engaged in the production and sale of agricultural products, one of which is the managing company (parent company), and the rest are controlled subsidiaries (Markovina, Zorin & Ostaev, 2018).

Many domestic scientists are involved in evaluating the effectiveness of the management of organizations and enterprises (Lyubushin, 2010; Sheremet, 2009). Issues of efficiency in management accounting and analysis are also given attention by individual authors (Alborov, Kontsevaya & Livenskaya, 2013; Kostyukova, Bobryshev, 2016; Alborov, Kontsevaya, Klychova & Kuznetsovd, 2017). The leading world powers are fighting for technological leadership and increasing the efficiency of their innovative systems, however, Foresight studies for these purposes have been considered by many domestic and foreign authors (Trukhachev, Kriulina & Tarasenko, 2008; Dalkey, Helmer-Hirschberg, 1962; Loveridge, Georghiou & Nedeva, 1995).

Foresight research in management accounting received little attention, respectively, this area requires more in-depth research.

Since there are a lot of indicators for assessing sustainable development in management accounting at the moment, there is a need for the formation of a comprehensive system of indicators for the sustainable development of agricultural enterprises included in the agricultural holding.

Management accounting in agricultural production should take into account all industry specifics and fundamental approaches of the economic entity and should also be aimed at improving the food security of the country (Savitskaya, 2007).

The country's food security depends not only on agricultural production and product processing, but also on innovative research approaches for agricultural development (Kokonov, Ostaev, Valiullina, Ryabova, Mukhina, Latysheva & Nikitin, 2019; Frantsisko, Ternavshchenko, Molchan, Ostaev, Ovcharenko & Balashova, 2020; Arbeláez-Campillo, Rojas Bahamón, 2020).

Methodology

Management accounting should solve all strategic tasks that require system analysis (Ostaev, Gogolev, Kondratev, Markovina, Mironova, Kravchenko & Alexandrova, 2019; Ostaev, Khosiev, Nekrasova, Frantsisko, Markovina & Kubatieva, 2019). Foresight research in management accounting should be developed according to a certain scheme and logic.

We believe that it is necessary to assess the problem areas in the Foresight study in management accounting, which are subject to study, analysis of current trends, and trends that in the future will play a significant role in the functioning of the economic entity (s).

Based on this, Foresight research in management accounting is a set of expert forecasting methods and approaches for developing solutions for the future functioning of an economic entity (entities) in the long term.

Factors affecting economic markets or economic relations are identified (determined) in Foresight studies in management accounting. Foresight research management accounting specialists must be aware of how the existing financial and economic markets will change, which products or business services will be most in demand in these markets, which technological solutions will be needed to provide such services or products in order to be successful and competitive in business.

In addition, it is necessary to determine exactly what steps must be taken so that these technological solutions are implemented in the economic life of an economic entity (Ostaev, Gogolev, Kondratiev, Markovina, Mironova, Kravchenko & Aleksandrova, 2019). Certain growth trends (technology, production, economics, etc.) will be identified after studying all the connecting factors from beginning to end (Popper, Wagner & Larson, 1998). The company will have to concentrate on growth trends and build its linear system of accounting and management positions, which the economic entity will target and will spend its resources on a priority. Selected accounting and managerial positions should be based on competent research, and economic and technological roadmaps should be built for these priority positions.

A roadmap for management accounting is an illustrated representation of the development of several scenarios for the release and sale of a new product; technological development, or a modernized old product, taking into account all the requirements, development of a separate industry.

In addition to the accounting and management apparatus (personnel), competent experts (businessmen, scientists, managers, etc.) should participate in Foresight studies. There can be an unlimited number of experts, while the degree of involvement of these experts can be different (questioning, monitoring, analysis, interviews - face-to-face meetings, participation directly in the work of the expert group, etc.). Foresight studies depend on the methods used for forecasting, monitoring, analysis, etc., as well as the allocated budget for this project.

Foresight studies for management accounting should use many different research methods. Methods of management accounting in Foresight research should be evidence-based, expert, creative, taking into account interaction with all methods of integrated and strategic analysis, management, accounting, forecasting, budgeting and planning.

Table 1. Special methods for Foresight Research (Martin, 1993).

.PNG)

Results

Usually Foresight begins where traditional planning and budgeting in management accounting ends (Maslennikov, Shmeleva, 2014; Kontsevaya, Alborov, Kontsevaya & Makunina, 2019). For example, the term traditional planning and budgeting in management accounting can be a year, two or three (Kovaleva, Rusetskiy, Okorokova, Antoshkina & Frantsisko, 2018). Foresight research in management accounting should be focused on a long period, but in the modern world everything is transient and variable, therefore any research requires tactical adjustments for the entire research period.

The specific development of the economy of a business entity, business entities or an individual area is studied as a whole with the help of Foresight studies for management accounting purposes. Finally, Foresight in management accounting today should be actively used for forecasts of the development of various industries: from agriculture to nanotechnologies and banking.

It is known that innovations can be promoted by the method of technological impetus, which is based on development, or use the method of market attraction when the company focuses on the market (Popper, 2012). Foresight research in management accounting, of course, is based on modern technologies, focusing on the future, but markets and factors determining the demand for strategic technologies play a decisive role.

Foresight studies for management accounting primarily take into account evidence-based methods: relying on serious data, a deep systematic analysis of trends (Ostaev, Klychova & Nekrasova, 2018; Sheremet, 2009). Foresight studies also analyze research fronts, these are areas of science and technology in which explosive citation growth is planned (the first sign that a technological breakthrough may occur here) (Popper, 2007).

In addition, instead of attracting a large number of experts, artificial intelligence can be used more actively. However, research cannot be done without people; people still have the right to make managerial decisions. Successful projects of recent years have been based on integrated approaches that allow creating methodological models for different types of Foresight (Popper, 2012).

The methodological model of the Foresight project is developed specifically to perform specific tasks, taking into account available resources and potential. It is necessary to take into account the functions of each method during the entire study, and the ways in which these methods can be synthesized and combined to maximize the overall economic effect (Loveridge, Georghiou & Nedeva, 1995).

There is no “ideal” methodological structure that would provide an optimal combination of methods, just as there is no “ideal” number of methods that should be used when performing the Foresight study (Martin, 1993).

The practice of Foresight has shown that it is important not only to determine a successful combination of methods, but also to skillfully combine them with each other, to use them in a sequence that will provide effective collection and analysis of information to develop predictive recommendations and solutions (Loveridge, 2001).

The methodological base used in Foresight research in management accounting should be adapted to meet the specific goals and objectives of the project, taking into account available resources, budget and capabilities of the economic entity (Kondratiev, Ostaev, Osipov, Bogomolova, Nekrasova & Abasheva, 2020). On its basis, a methodological model of a specific study should be formed.

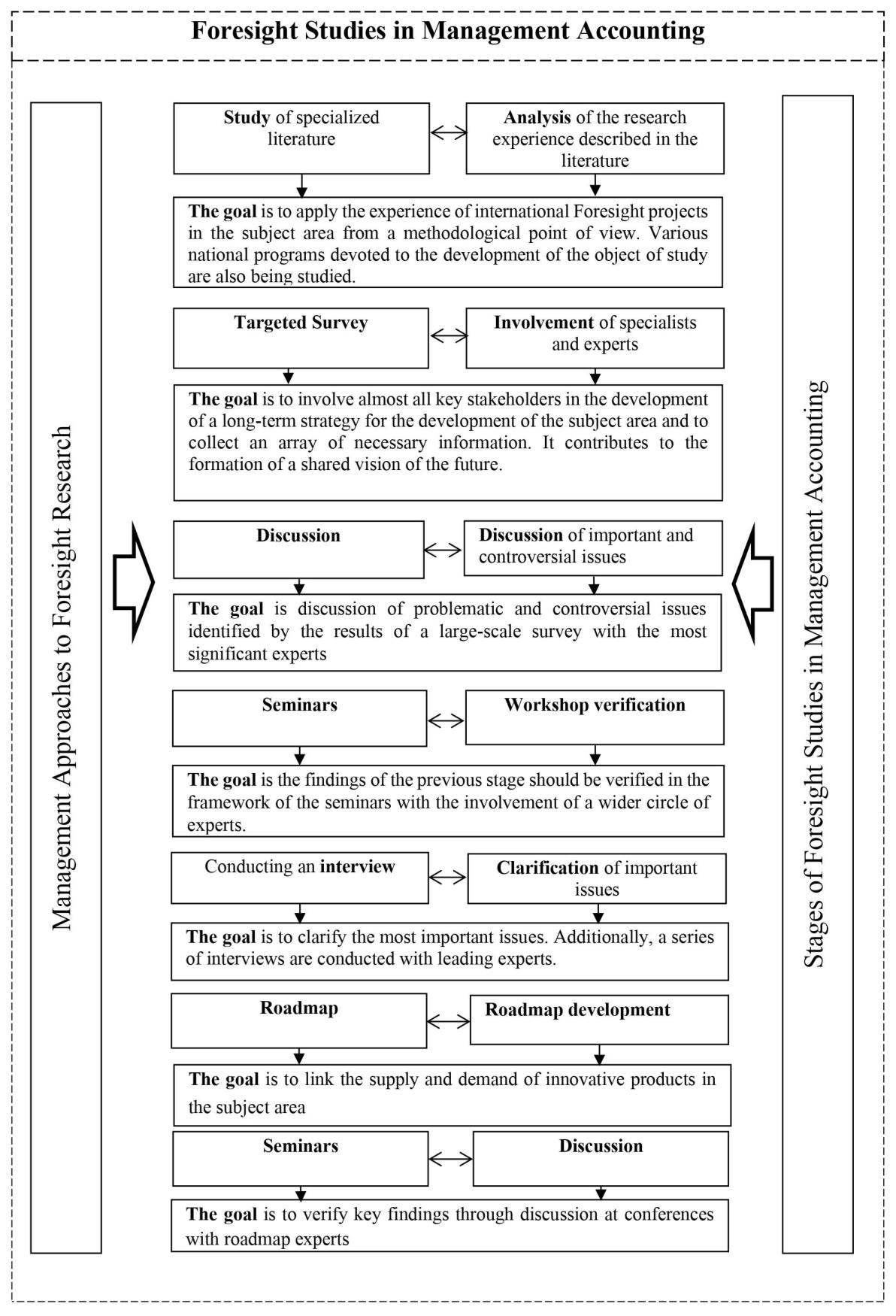

There are basic models for conducting Foresight studies that are applied at the corporate industry level; we suggest that the study be conducted according to the scheme shown in Figure 1 for management accounting purposes.

Figure 1. Foresight studies for management accounting and decision making (compiled by the authors).

An essential role in the Foresight process is played not only by the study of possible changes, but also by the degree of willingness of its participants to contribute to their implementation. From this point of view, the formation of two models of research and the behavior of stakeholders is observed: evolutionary and provocative (Popper, Wagner & Larson, 1998).

The foresight of the first model is aimed at improving and optimizing the existing system, and politicians are partners because they are interested in its effectiveness and development on a global scale.

World practice has developed basic models on the basis of which the construction of the Foresight process is possible:

- A long-term forecast for the development of research and development;

- market development and changing consumer demand;

- points of technological growth;

- processes of structural change in the business sector;

- scanning and monitoring.

The foresight of the second model is more radical. The focus can be on more fundamental changes, since it is believed that the existing paradigms do not correspond to new circumstances and it is necessary to create a new system on a completely different basis. The application of this approach leads to significant changes in management practice. Foresight studies, the results of which indicate the need for such a transformation, can create conflicts and need active supporters who understand that their organizations or industries need radical changes (Popper, Wagner & Larson, 1998; Popper, 2007).

The second Foresight model is currently being developed, since problems arise during the long-term forecast almost always associated with the invariability of the managerial model of an organization or department that developed many years ago. In addition, many of the problems today are “interdepartmental” and require orientation of the activities of government bodies towards achieving long-term priorities and making appropriate changes to the procedures for their activities, for example, establishing links between departments, reviewing areas of responsibility in situations where coordinated actions and activization are necessary and expanding contacts with non-governmental organizations (Maslennikov, Shmeleva, 2014).

Thus, the traditional methods of Foresight begin to be closely intertwined with the methods of accounting and management (Kokonov, Ostaev, Valiullina, Ryabova, Mukhina, Latysheva & Nikitin, 2019).

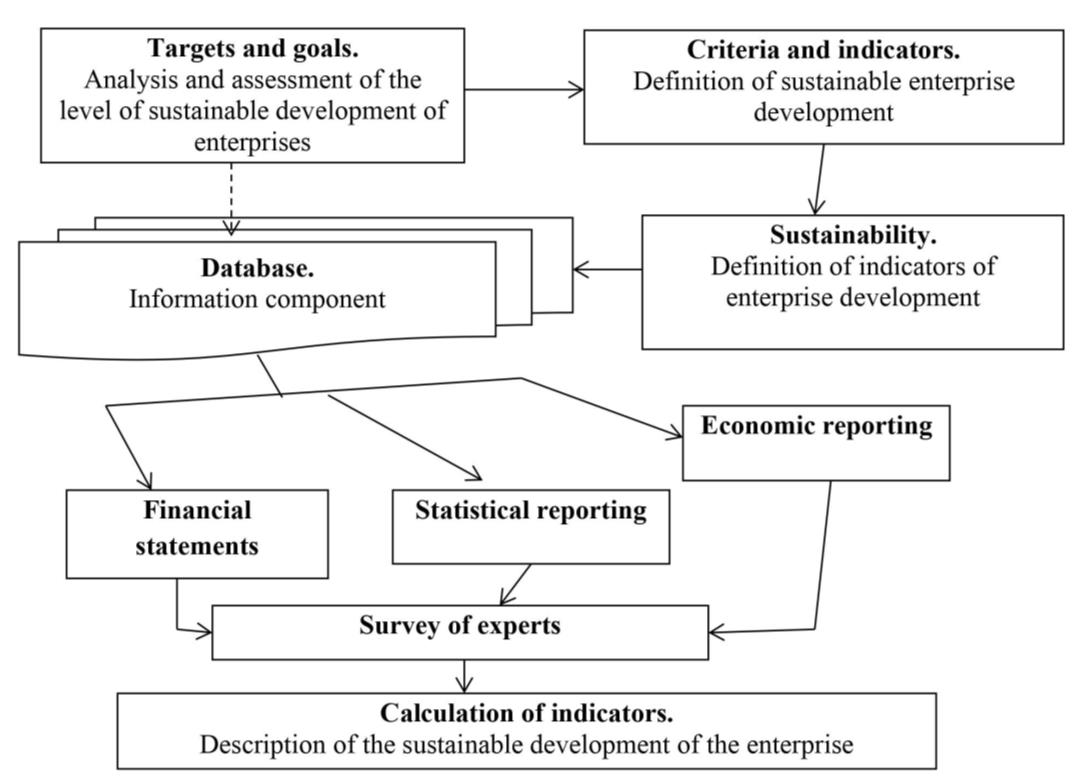

A comprehensive system of indicators for the sustainable development of agricultural enterprises should be formed in Foresight studies of management accounting of an agricultural holding.

It is advisable in this management accounting system for the purposes of Foresight:

1) use indicators reflecting the impact on the economic, social and environmental components of sustainable development;

2) apply indicators for the calculation of which information is required, which is reflected in the accounting, statistical and economic reporting of enterprises;

3) use indicators that take into account the specifics of the agricultural industry.

This will allow creating in management accounting a system of indicators with a sufficient breadth of coverage of all aspects of sustainable development of agricultural enterprises included in the agricultural holding.

To select indicators, it is most advisable to use an expert method in management accounting, that is, based on the opinion of specialists in the agricultural industry.

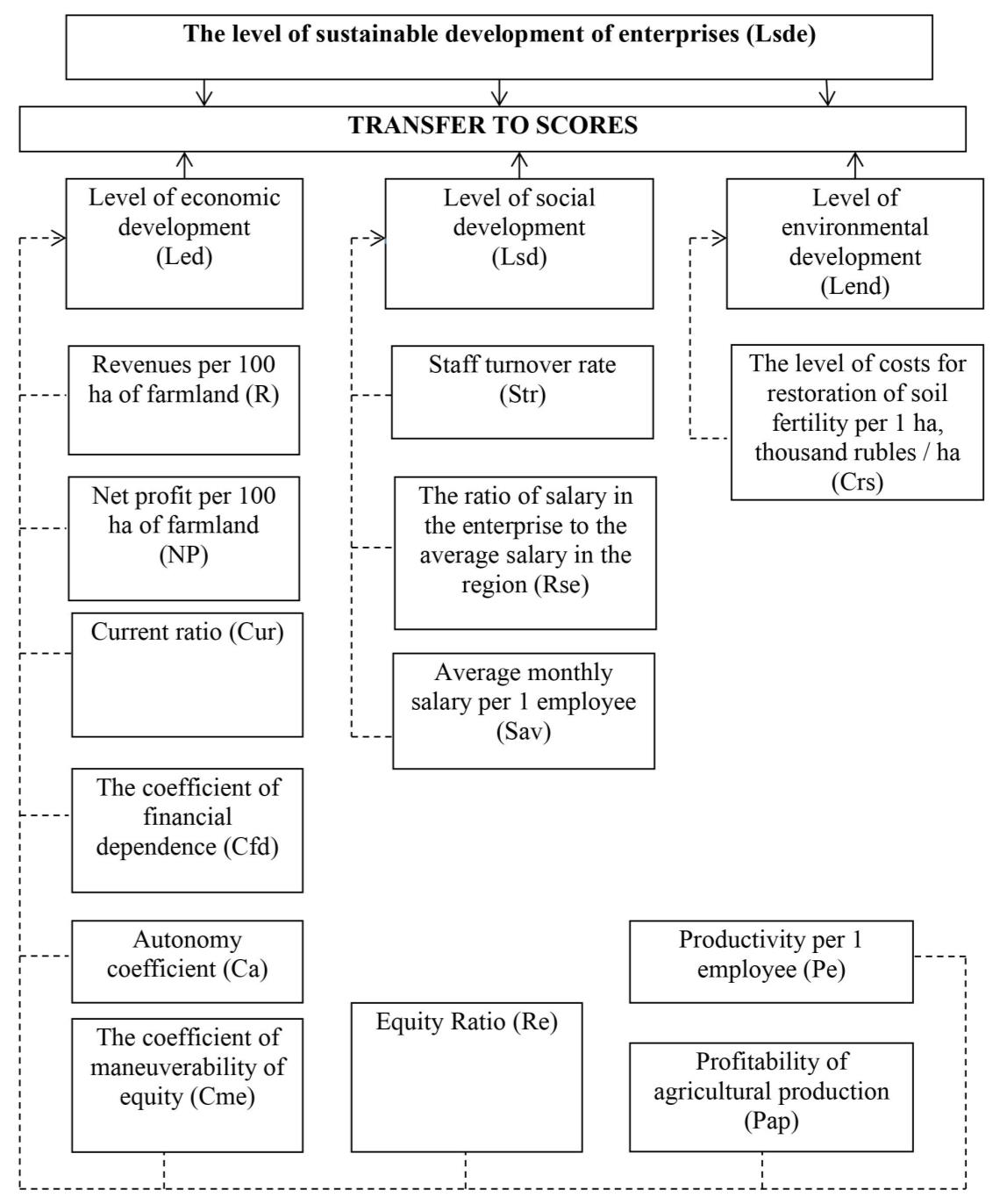

The formation of a system of indicators of sustainable development for management accounting is presented in Figure 2.

Figure 2. Formation of a system of indicators of management accounting for calculating the level of sustainable development of the enterprise (compiled by the authors).

For an expert survey, management accounting specialists developed a questionnaire in which the indicators proposed for selection are divided into 3 groups (economic, environmental, social), in each of which private indicators are presented.

It is necessary to evaluate these indicators on a 9-point scale, thereby indicating the degree to which each indicator reflects the level of sustainable development of an agricultural enterprise.

1 point this indicator does not at all reflect the level of sustainable development of an agricultural enterprise, and 9 points this indicator clearly reflects the level of sustainable development of an agricultural enterprise.

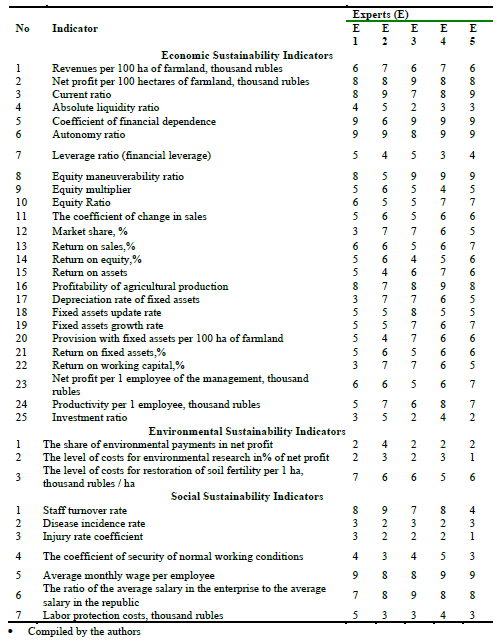

The matrix of questions and answers of experts is presented in table 2.

Table 2. Matrix of questions and answers of experts.

Five experts participated in the assessment of sustainable development indicators, who are managers and specialists of agricultural enterprises.

The matrix of questions and answers of experts is presented in table 3.

Table 3. Matrix of questions and answers of experts.

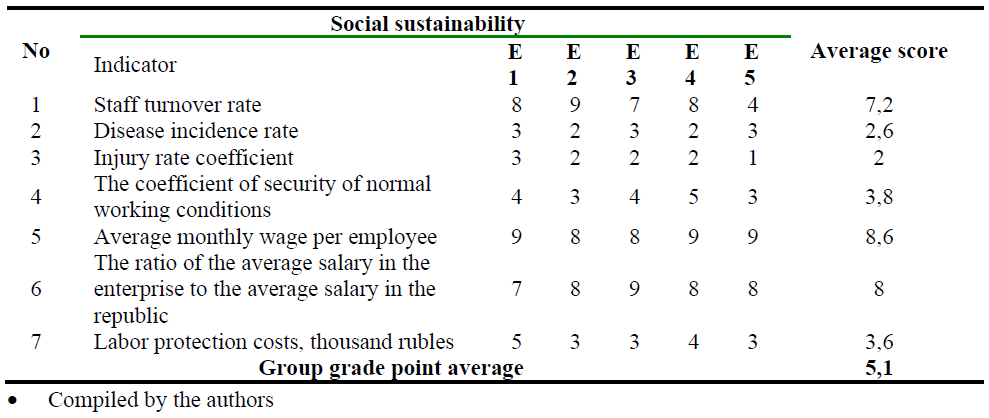

Based on the responses received, each group selected those indicators that, according to experts, most clearly and accurately reflect the sustainable development of the enterprise. The average score of the degree of reflection of each indicator and the average score in the group was determined for this.

Indicators whose value is above the group average and will be included in the indicator system for assessing the sustainable development of agricultural enterprises.

An example of determining social sustainability indicators that will be included in the system to assess the level of sustainable development is presented in table 4.

Table 4. Calculation of the average score of the reflection degree of the indicator for the social component of sustainable development.

Since indicators have different calculation formulas and units, we suggest using a point system to bring these indicators into a comparable form. At the same time, we take into account the direction the indicator affects the sustainable development of the enterprise. In the case of an increase in the direction of the indicator's influence on sustainable development (i.e., the higher the better), we take 10 points for the maximum value. In the case of a decrease in the direction of the indicator's influence on sustainable development (i.e., the lower the better), we take 10 points as the minimum value.

Based on the data obtained by experts, we suggest assessing the level of sustainable development of the main agricultural enterprises using the methodology presented in Figure 3 and the indicator system presented in Figure 4.

Figure 3. Construction of a generalized indicator of sustainable development of agricultural enterprises (compiled by the authors).

Figure 4. The system of indicators for sustainable development of agricultural enterprises (compiled by the authors).

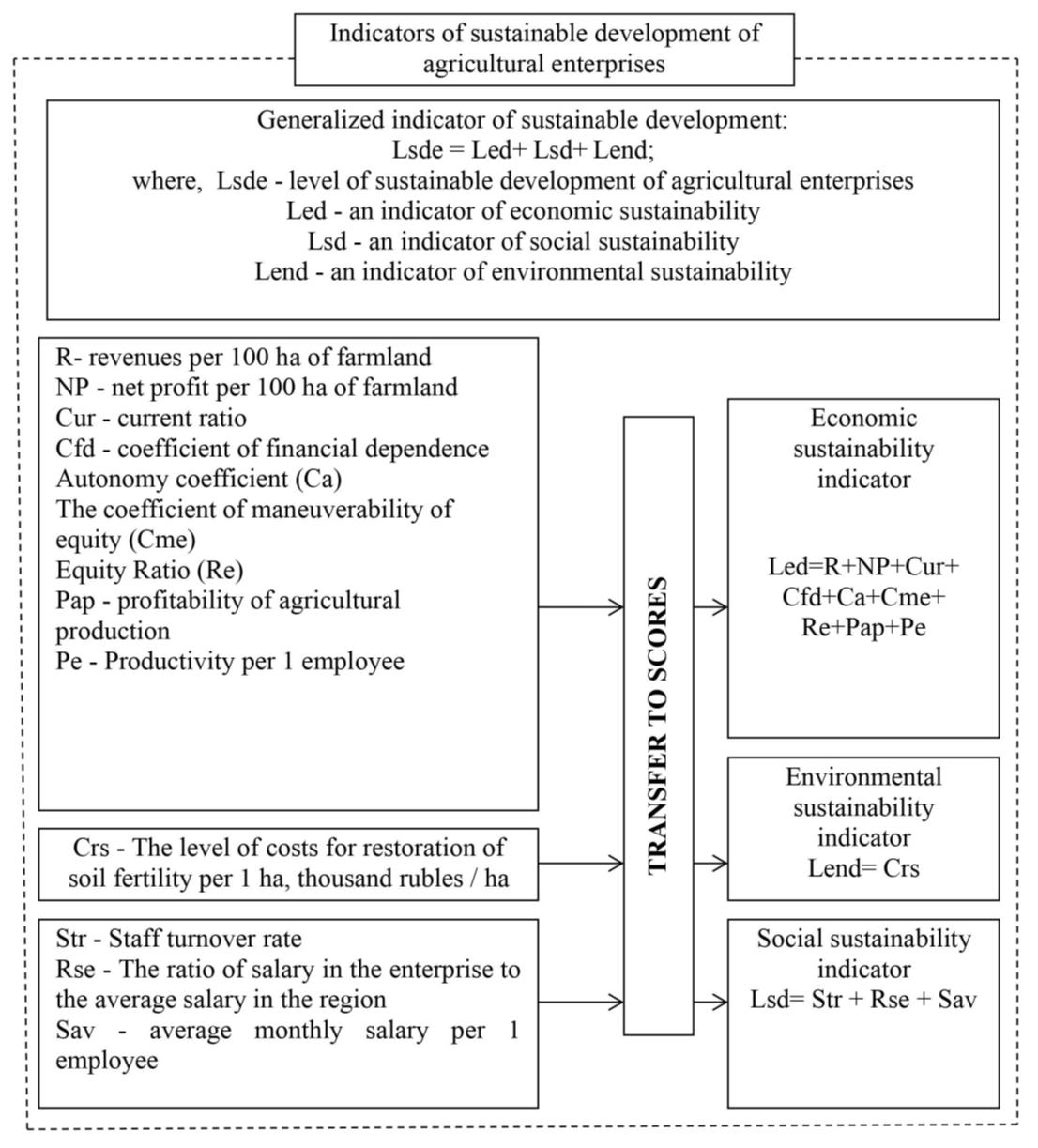

Thus, we will calculate the generalized indicator of the level of sustainable development of agricultural enterprises according to the following formula:

Lsde= Led+Lsd+Lend (1),

We propose to interpret the generalized indicator of sustainable development of enterprises according to the following table 5.

Table 5. Interval values for determining the state of development of enterprises.

Since the maximum number of points can be equal to 130 (13 indicators * 10 points), and the minimum - 0, the interval step is determined by the formula:

![]()

where ![]() and

and ![]() is the smallest and greatest value of the grouping attribute

is the smallest and greatest value of the grouping attribute

![]() -; the number of intervals.

-; the number of intervals.

![]()

We take h = 43.3 for the upper boundary of the first interval. This value is also the lower boundary of the second interval. Adding the interval (h) to it, we determine the upper boundary of the second interval: 43.3 + 43.3 = 86.6. Similarly, we determine the boundaries of the third interval.

Having calculated a comprehensive indicator of sustainable development of enterprises, it is possible to conduct a comparative analysis to identify more developed enterprises of the holding.

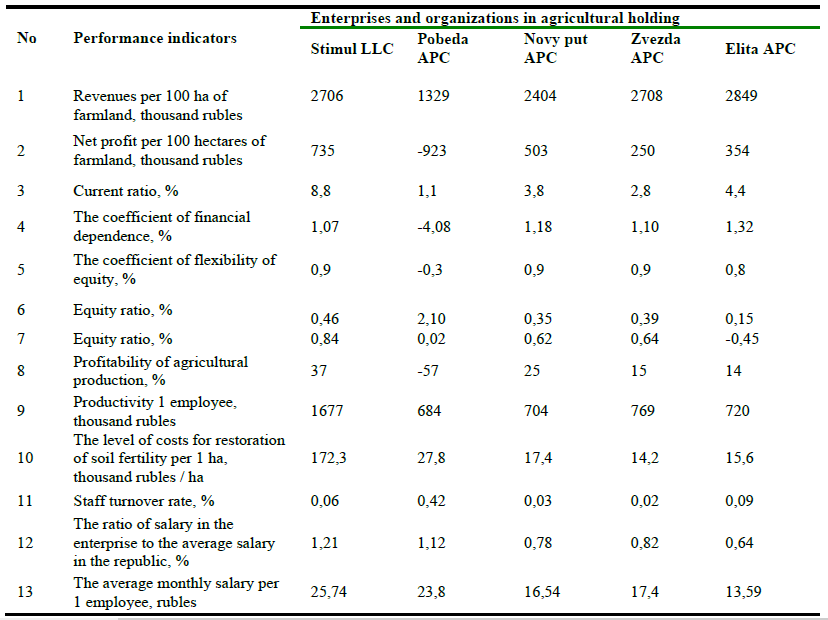

We will conduct research on 5 organizations and enterprises included in the holding: Stimul LLC, Pobeda APC, Novy put APC, Zvezda APC, Elita APC.

To carry out the calculation of indicators of the economic, environmental and social components of sustainability, as well as to calculate a generalized indicator of the level of sustainable development of agricultural holding enterprises, the initial information presented in table 6 is required. The calculated indicators are converted to points (table 7). Table 8 calculates the social, economic and environmental indicators characterizing the sustainable development of the agricultural enterprises of the holding, as well as a generalized indicator of the level of sustainable development.

Table 6. The source data on the agricultural enterprises of the holding to calculate the indicator of sustainable development.

Table 7. The initial data on the agricultural enterprises of the holding to calculate the indicator of sustainable development (in points).

.PNG)

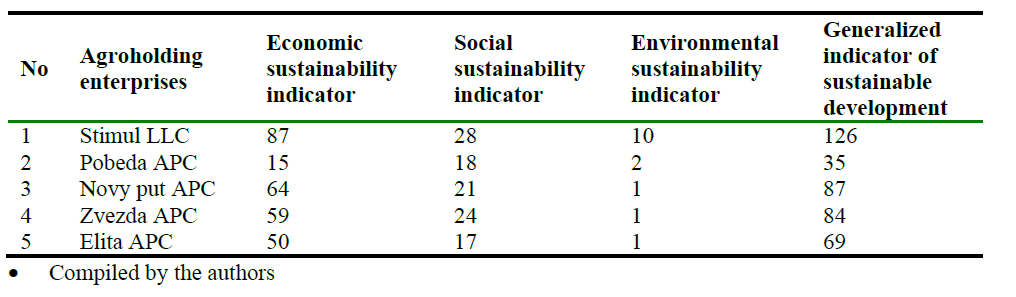

Table 8. Assessment of the level of sustainable development of agricultural enterprises of the holding.

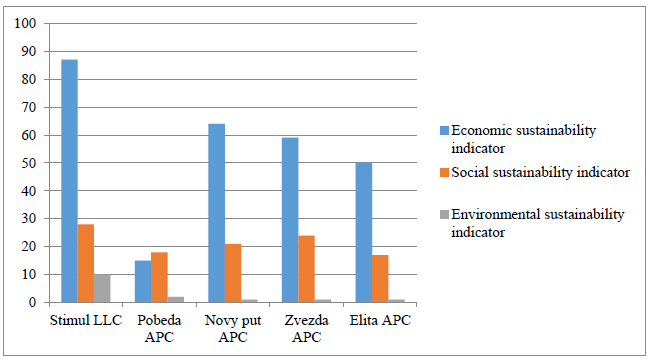

To clearly reflect the level of sustainable development of the holding enterprises, we will present it graphically.

Figure 5. The level of sustainable development of agricultural enterprises of the agricultural holding (compiled by the authors)

Conclusions

Based on the calculated indicators characterizing the sustainable development of the agricultural enterprises of the holding, it can be noted that Stimul LLC and Novy Put APC are at the highest level, these enterprises have sustainable development, while Stimul LLC is superior to other enterprises and has significant a margin in almost all indicators of sustainable development.

Consequently, the agricultural holding needs to stimulate lagging enterprises to bring them, as far as possible, to sustainable development, and bring additional income.

The proposed Foresight research methodology in management accounting will allow the formation of a comprehensive system of indicators for the sustainable development of agricultural enterprises of an agricultural holding. This technique also contributes to the adoption of managerial decisions promptly, which will allow us to develop specific mechanisms for managing business processes according to the intended forecast scenario of the agricultural holding.